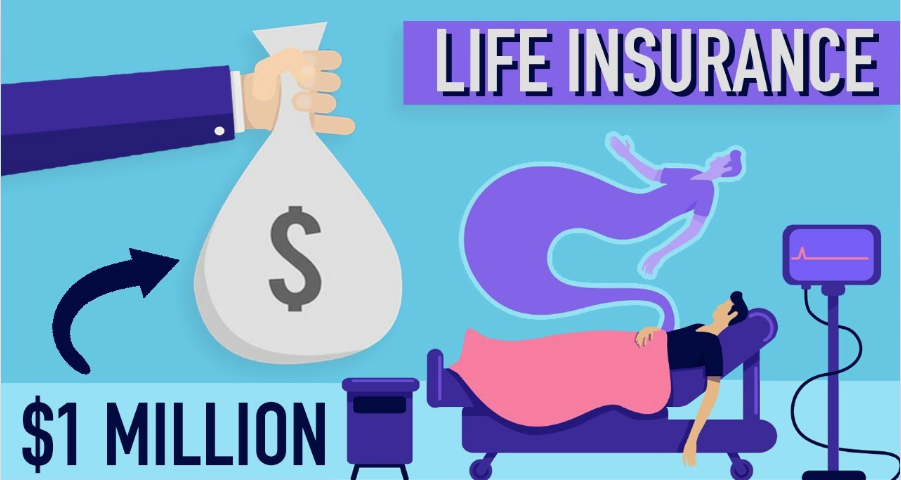

Life insurance work provides financial protection to beneficiaries upon the policyholder’s death. It involves paying regular premiums in exchange for a payout.

Understanding how life insurance works is key to securing your loved one’s financial future. This form of insurance is a contract between you and an insurance company. You pay monthly or annual premiums, and in return, the insurer promises to pay a sum of money to your designated beneficiaries after your passing.

The purpose of life insurance is to ease the financial burden on your family, ensuring they are covered for expenses like funeral costs, outstanding debts, and daily living costs. It’s a pivotal component of long-term financial planning, offering peace of mind knowing that your loved ones will have monetary support during difficult times. Life insurance work With various types of policies available, choosing the right one hinges on your personal needs, financial goals, and the security you wish to provide for your family.

The Basics Of Life Insurance

Table of Contents

Life insurance is a contract. It promises to pay money when someone dies. This money helps those who depend on that person. It can pay bills, loans, and other costs.

The Principle Behind Life Insurance

A person pays a little money, called a premium, regularly. The insurance company collects these premiums. It pays out a big sum, known as the death benefit, later. This happens when the person who has the insurance passes away. The money goes to the people named in the policy, called beneficiaries. It is a form of financial safety for families.

Types Of Life Insurance Policies

- Term Life Insurance:

This is for a set time, like 10 or 20 years. If the person dies at this time, beneficiaries get money. If not, the policy ends. - Whole Life Insurance:

This policy lasts a lifetime. It also builds up a cash value over time that one can borrow from. - Universal Life Insurance:

Similar to whole life but more flexible. It allows policyholders to adjust their premiums and death benefits.

| Type of Policy | Duration | Cash Value | Flexibility |

|---|---|---|---|

| Term Life | Fixed | No | No |

| Whole Life | Lifetime | Yes | No |

| Universal Life | Lifetime | Yes | Yes |

Determining The Coverage You Need

Understanding life insurance starts with knowing how much coverage suits your life. Every person’s needs differ. In ‘Determining the Coverage You Need,’ we’ll guide you through this process.

Assessing Your Financial Situation

Grasping your current financial status is crucial. It sets the stage for spotting the coverage scope necessary to protect loved ones. Begin with basic questions:

- What debts are present? Think mortgages, loans, and credit cards.

- Savings and investments: Include retirement accounts and stocks.

- Income: Note your earnings and other income streams.

These insights help sketch a dependable financial picture. That’s key in pinpointing the amount of life insurance you need.

Calculating Future Obligations

Next, factor in future financial responsibilities. These range from kids’ education to daily living costs. Ponder these areas:

| Future Expense | Estimate Cost |

|---|---|

| Children’s Education | Tuition, books, etc. |

| Retirement Savings | Needed for spouse’s comfort. |

| Emergency Fund | Unexpected cost coverage. |

| Final Expenses | Funeral and estate taxes. |

Calculate a total sum that’ll encompass these future obligations. This figure, combined with your current financial status, guides the coverage amount.

Choosing The Right Policy

Finding the best life insurance policy can seem daunting. Life insurance safeguards your loved ones’ future. With many plans available, the key lies in understanding the options. The perfect policy balances coverage needs, budget, and long-term financial goals. Let’s explore how to navigate these choices.

Term Life Insurance Versus Permanent Life Insurance

Term life insurance provides coverage for a specific period. It’s like renting insurance. If the policyholder passes away within this period, beneficiaries receive the death benefit. It does not accumulate cash value.

Permanent life insurance, on the other hand, lasts a lifetime. It’s like buying insurance. Besides the death benefit, these policies often build cash value over time. This cash can be a resource for loans or withdrawals.

| Term Life Insurance | Permanent Life Insurance |

|---|---|

| Fixed term (e.g., 10, 20, 30 years) | Lifetime coverage |

| No cash value | Accumulates cash value |

| Lower initial premiums | Higher premiums but can grow investment |

Factors To Consider When Selecting A Policy

- Coverage Duration: Align your coverage with long-term financial plans.

- Cost: Ensure premiums fit comfortably within your budget.

- Financial Goals: Use the policy as a tool to achieve future objectives.

- Health Status: Premiums can vary greatly based on your health.

- Benefit Amount: Decide on the sum that will protect your family’s needs.

- Policy Features: Look for flexible features that cater to change over time.

Research is your ally in selecting a life insurance policy. Advisors can help, but personal needs guide the final choice. Choose a plan that offers peace of mind and financial security for those you care about.

The Process of Underwriting

Underwriting is a key step in getting life insurance. It’s how insurers decide if they can insure you. They look at how risky it is to give you insurance. This process can be complex. Let’s break down what happens during underwriting.

Risk Assessment And Health Evaluations

Risk assessment is about figuring out your insurance risk. Insurers check many things about you. They want to know your age, job, lifestyle, and health. This helps them predict your life length.

- Age: Younger people often get better rates.

- Job: Safer jobs may mean lower premiums.

- Lifestyle: Smoking or adventure sports can raise your cost.

- Health: Good health usually equals lower prices.

The Role of Medical Exams In Underwriting

Medical exams are important to underwriting. They give a clear picture of your health. This can include blood tests, blood pressure checks, and more. If your health is good, your insurance might cost less.

| Test | Purpose | Impact on Insurance |

|---|---|---|

| Blood Test | Check for health issues. | Can affect your rates. |

| Blood Pressure | Assess heart risk. | High pressure may increase premiums. |

| Weight Check | Gauge overall health. | Over or underweight can change costs. |

Paying For Life Insurance

Life insurance provides financial security for loved ones. Part of owning a policy involves understanding and managing payments. From premiums to payment plans, it’s essential to know your options.

Understanding Premiums

Premiums are regular payments to keep life insurance active. Think of them as a subscription fee for your coverage. Paying premiums on time is crucial.

- Factors affecting premiums include age, health, and coverage amount.

- Typically, younger policyholders pay less.

- A medical exam may lead to lower premiums if healthy.

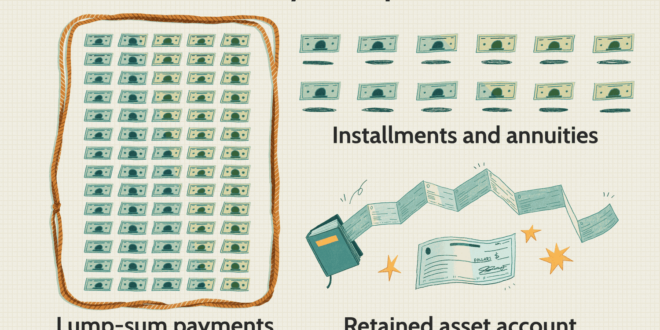

Options For Payment Plans

Choosing a suitable payment plan ensures premiums fit your budget. Life insurance companies offer flexibility in how and when you make payments.

| Payment Frequency | Pros | Cons |

|---|---|---|

| Monthly | Smaller, manageable payments | The higher total annual cost |

| Annually | Discounts for one-time payment | Larger lump sum |

Policy Riders And Additional Benefits

Life insurance is not just a promise for the future.

It can also offer unique options through Policy Riders and Additional Benefits.

Think of riders as custom parts you can add to a car.

They make your insurance policy more useful to you and your loved ones.

Common Riders Explained

Riders are extra features you can add to a life insurance policy.

Some protect you while you are still alive.

Some can even return your premiums if you outlive the policy.

- Waiver of Premium Rider: If you get sick or hurt and can’t work, this rider means you don’t have to pay your premiums anymore.

- Accidental Death Benefit Rider: If an accident happens and you pass away, this rider gives extra money to your family.

- Guaranteed Insurability Rider: This rider allows you to add more insurance later without a health check-up.

Customizing Your Coverage

Adding riders can create a safety net tailored to your needs.

Think about what worries you in life.

Pick riders that address those concerns.

Your family gets peace of mind.

You get a policy that fits like a glove.

Each rider has a small cost.

But the benefits can be big during tough times.

| Rider Name | What It Does |

|---|---|

| Critical Illness Rider | Pays a lump sum if you get a serious illness. |

| Term Conversion Rider | Lets you switch to permanent insurance without a new health exam. |

| Child Term Rider | Adds temporary insurance for your kids. |

Filing A Claim And Beneficiary Procedures

Understanding the process involved in filing a claim and the responsibilities of beneficiaries is crucial when navigating life insurance. When a policyholder passes away, beneficiaries must act to receive the policy’s benefits. Properly following each step ensures a smooth transaction and timely access to the insurance proceeds.

Steps For Filing A Life Insurance Claim

Filing a life insurance claim involves a few key steps:

- Obtain Death Certificate: Secure multiple copies of the official death certificate.

- Contact Insurance Company: Inform the insurer about the policyholder’s passing as soon as possible.

- Complete Claim Forms: Fill out the necessary paperwork provided by the insurance company.

- Submit Required Documents: Attach the death certificate and any other requested documentation.

- Review Process: The insurance company reviews the claim to ensure policy terms are met.

- Receive Payment: Upon approval, funds are disbursed to the beneficiaries.

Responsibilities of The Policy Beneficiaries

Beneficiaries hold several responsibilities:

- Communicate Promptly: Contact the insurer without delay when the policyholder dies.

- Document Management: Safely keep all documents related to the policy and claim.

- Claim Accuracy: Ensure all information on claim forms is exact and truthful.

- Understand Payout Options: Be aware of different payout methods and pick the best one.

- Facilitate Process: Respond to insurer inquiries and requests swiftly.

- Report Issues: Notify the insurer of any problems or concerns during the claim process.

Tax Implications And Life Insurance

Understanding life insurance involves knowing its tax aspects. Taxes can affect the benefits your loved ones receive. This section covers how life insurance policies interact with taxes.

Tax Benefits of Life Insurance

Life insurance offers notable tax advantages:

- Death benefits are usually tax-free. Beneficiaries typically don’t pay income tax on money they receive.

- Premiums are not tax-deductible. You pay these with after-tax dollars.

- Cash value growth is tax-deferred. In permanent policies, cash value grows without current tax.

- Loans taken may be tax-free. Borrowing from the policy’s cash value isn’t considered taxable income.

Understanding Potential Tax Liabilities

Some situations may lead to tax on life insurance:

| Scenario | Tax Impact |

|---|---|

| Estate inclusion | Large policies may create estate taxes. |

| Policy surrender | Cashing out can bring taxable income. |

| Company-owned policies | Corporate-owned life insurance may face different tax rules. |

Reviewing And Updating Your Policy

Understanding how to keep your life insurance policy up to date is crucial. Life is full of changes, and your policy should reflect that. Regularly reviewing and updating your coverage ensures that your policy remains aligned with your current needs and goals. Let’s dive into why and when you should reevaluate your coverage, and how life changes can impact your insurance needs.

When To Reevaluate Your Coverage

Knowing the right time to reexamine your life insurance policy is key. Consider these milestones:

- Annual Review: At least once a year, glance over your policy.

- Major Life Events: Marriage, divorce, childbirth, or buying a home trigger a review.

- Financial Changes: A significant increase or decrease in your income means an update.

- Career Moves: Starting a business or changing jobs can alter your coverage needs.

The Impact of Life Changes On Insurance Needs

Significant life events might change what you require from your life insurance. Here’s how:

| Life Event | Impact |

|---|---|

| Marriage | Consider increasing your coverage to support your spouse. |

| Baby | Update your policy to protect your growing family’s future. |

| Homeownership | Your coverage amount should help pay off your mortgage if needed. |

| Retirement | You may reduce your coverage as your dependents’ needs decrease. |

Remember to adjust your beneficiary information after any life change. This ensures the right people receive your policy’s benefits. Bear in mind the impact of debts and future educational expenses for your children as well.

Common Misconceptions About Life Insurance

Life insurance is an agreement that can seem complicated. Many people hear false info. They may think life insurance does not serve them well. This section helps clear up some common wrong ideas.

Demystifying Life Insurance Myths

It’s crucial to know myths are not facts. Let’s clear them up:

- Myth 1: “Only breadwinners need it.” In truth, costs can hit anyone.

- Myth 2: “It’s too costly.” Options exist for all budgets.

- Myth 3: “Young people can skip it.” The best rates go to the young.

- Myth 4: “It’s all the same.” Plans differ and can be tailored.

The Truth About Life Insurance Policies

Understanding real facts about life insurance is key:

| Misconception | Reality |

|---|---|

| Can’t be changed once purchased. | Policies may be adjustable. |

| Only useful when you pass away. | Some plans offer living benefits. |

| Only for final expenses. | Can cover lost income, debts, and more. |

| Unused premiums are a loss. | Some policies accrue a cash value. |

Frequently Asked Questions Of How Does Life Insurance Work

What is life insurance?

Life insurance is a contract between an individual and an insurance provider. In exchange for premium payments, the provider pays a designated beneficiary a sum of money upon the death of the insured person.

How do life insurance premiums work?

Premiums are the payments you make to keep your life insurance policy active. They can be paid monthly, quarterly, or annually and are determined by factors including your age, health, and the policy’s value.

What are the main types of life insurance?

The two primary types of life insurance are term life, which covers you for a specified period, and whole life, which offers lifelong coverage and includes a cash value component.

Can I withdraw money from life insurance?

Some life insurance policies, particularly whole life and universal life, accumulate cash value that you can borrow against or withdraw; however, this can reduce the death benefit.

Conclusion

Understanding life insurance is crucial for financial security. It ensures peace of mind, protecting loved ones from economic strain. By choosing the right policy and coverage, you can tailor it to your unique needs. Ensure you review terms regularly and consult with a professional.