In addition to private disability insurance, Disability Insurance In USA the United States has a federal program called Social Security Disability Insurance (SSDI). SSDI provides benefits to individuals with disabilities who have paid into the Social Security system Disability Insurance In USA through payroll taxes.

It’s important for individuals to carefully review and understand the terms and conditions of their disability insurance policies. Disability insurance can be a critical financial safety net in the event of a disability, Disability Insurance In USA helping individuals and their families maintain their financial stability during challenging times.

Certainly

Disability Insurance In USA

I can provide information about disability insurance in the United States in English.

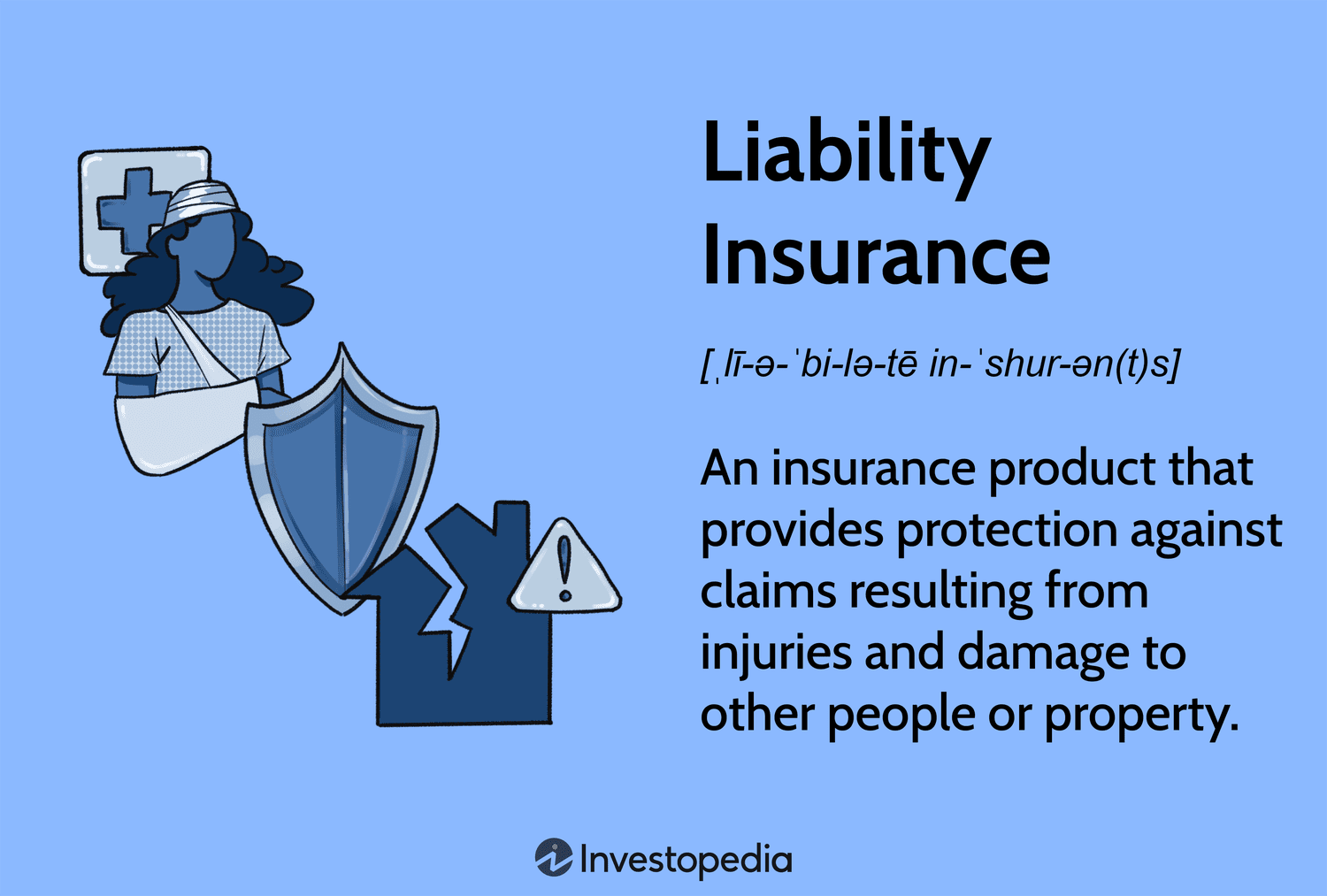

Disability insurance, often referred to as DI or disability income insurance, is a type of insurance coverage that provides financial protection to individuals who become unable to work due to a disability. It helps replace a portion of their income while they are unable to work, ensuring they can continue to meet their financial obligations.

Here are some key points about disability insurance in the United States:

Types of Disability Insurance:

Disability Insurance In USA

Short-Term Disability Insurance: This typically provides coverage for a short duration, often up to six months, and is designed to replace a portion of your income during a temporary disability.

Long-Term Disability Insurance: This provides coverage for an extended period, potentially until retirement age if needed, and is intended for more severe and long-lasting disabilities.

Sources of Disability Insurance:

Employer-Sponsored Plans: Many employers offer disability insurance as part of their employee benefits package. These plans can vary in terms of coverage and eligibility.

Individual Policies: Individuals can purchase disability insurance policies directly from insurance companies. These policies can be customized to meet specific needs but may be more expensive.

Coverage and Benefits:

Disability Insurance In USA

Disability insurance typically covers a percentage of your pre-disability income, often ranging from 50% to 70%.

The benefits received are generally tax-free if the premiums are paid with after-tax dollars.

The definition of disability can vary, but it usually involves being unable to perform your own occupation (own-occupation coverage) or any occupation (any-occupation coverage) due to a disabling condition.

Elimination Period:

Disability insurance policies often have an elimination period or waiting period before benefits kick in. This can range from a few days to several months, depending on the policy.

Benefit Duration:

The duration of benefits can vary, but long-term disability insurance policies can provide coverage for years, or even until retirement age if necessary.

Cost of Disability Insurance:

The cost of disability insurance premiums depends on factors such as age, health, occupation, income, and the level of coverage desired.

Social Security Disability Insurance (SSDI):

Qualifying for Disability Benefits:

To qualify for disability benefits, you typically need to meet certain medical and occupational criteria outlined in your policy. This often involves providing medical evidence of your disability.

Some policies also have a waiting period, known as the “elimination period,” during which you must be disabled before you can start receiving benefits.

Applying for Disability Benefits:

If you need to claim disability benefits, you’ll need to follow the application process outlined by your insurer. This typically involves submitting a claim form and supporting medical documentation.

It’s crucial to be honest and thorough in your application to ensure a smooth claims process.

Renewability and Guaranteed Renewability:

When purchasing an individual disability insurance policy, it’s important to understand whether the policy is non-cancelable and guaranteed renewable. A non-cancelable policy means that the insurer cannot change the terms or cancel the policy as long as you pay the premiums. A guaranteed renewable policy guarantees your ability to renew the policy but may allow for premium increases.

Occupational Classifications:

The cost and availability of disability insurance can also depend on your occupation. Some professions considered riskier or more physically demanding may have higher premiums.

Policy Riders:

Disability insurance policies often offer optional riders that can be added to the base policy for additional coverage. Common riders include cost-of-living adjustments (COLA) to account for inflation and residual disability riders that provide benefits if you can work but earn less due to your disability.

Reviewing and Updating:

As your life circumstances change, it’s important to periodically review your disability insurance policy to ensure it still meets your needs. For example, if you get a new job or experience an increase in income, you may want to adjust your coverage.

Social Security Offset:

Some disability insurance policies have a provision that offsets benefits by the amount you receive from Social Security Disability Insurance (SSDI). This is important to understand when calculating your overall disability income.

Legal Protections:

The United States has laws, such as the Americans with Disabilities Act (ADA), that protect individuals with disabilities from discrimination in employment and public services. Understanding your rights under these laws is important.

Seek Professional Advice:

Given the complexity of disability insurance policies and the significant financial implications, it’s advisable to consult with a financial advisor or insurance specialist when considering disability insurance options.

In summary, disability insurance in the United States is a vital tool for protecting your financial well-being in case you become unable to work due to a disability. Understanding the various aspects of disability insurance, from policy types to eligibility criteria, is crucial to making informed decisions about your coverage. Always read and review your policy carefully to ensure it aligns with your needs and financial goals.

Disability insurance in the United States is a type of coverage that provides financial protection to individuals who are unable to work due to a disability or illness. This insurance is designed to replace a portion of the insured person’s income if they become disabled and are unable to perform their job.

There are two main types of disability insurance in the U.S.:

Short-Term Disability Insurance (STD):

STD provides coverage for a limited period, usually ranging from a few weeks to a few months.

It typically replaces a percentage of the insured person’s salary, often around 60-70%.

It is often offered by employers as part of their employee benefits package.

Long-Term Disability Insurance (LTD):

LTD provides coverage for a more extended period, sometimes up to several years or until retirement age, depending on the policy terms.

The benefit amount can vary but often covers around 40-60% of the insured person’s pre-disability income.

It can be purchased individually or through an employer-sponsored plan.

Here are some key points to understand about disability insurance in the U.S.:

Eligibility: Eligibility criteria for disability insurance can vary depending on the insurance provider and the specific policy. Generally, individuals need to be employed and actively working to qualify for coverage.

Waiting Period: Many disability insurance policies have a waiting period, known as an elimination period, before benefits kick in. This period can range from a few days to several months after the onset of disability.

Coverage: Disability insurance covers a range of disabilities, including those caused by accidents, illnesses, or injuries. The specific conditions covered will be outlined in the policy.

Benefit Duration: Long-term disability insurance can provide benefits for an extended period, potentially until retirement age, while short-term disability insurance offers benefits for a shorter duration.

Premiums: Premiums for disability insurance can vary based on factors such as age, health, occupation, and the level of coverage chosen. Employer-sponsored plans often offer more affordable rates.

Taxation: The tax treatment of disability insurance benefits depends on how the policy is paid for. Employer-sponsored plans may have different tax implications than individually purchased policies.

Social Security Disability Insurance (SSDI): In addition to private disability insurance, the U.S. government offers Social Security Disability Insurance (SSDI) for individuals who meet specific criteria and have paid into the Social Security system. SSDI provides financial assistance to people with long-term disabilities.

It’s important for individuals to carefully review and understand the terms and conditions of their disability insurance policy, including the waiting period, benefit amount, and any exclusions or limitations. This coverage can provide crucial financial support in the event of a disability that prevents someone from working and earning an income.

Disability Insurance

Disability insurance, also known as income protection or disability income insurance, is a type of insurance that provides financial protection to individuals in the event they become disabled and are unable to work. This insurance is designed to replace a portion of the insured person’s income if they are unable to perform their job due to a disability.

There are several key aspects to disability insurance:

Types of Disability Insurance:

Short-Term Disability Insurance: This type of insurance typically covers disabilities that last for a few weeks to a few months. It provides a portion of the insured person’s salary during the disability period.

Long-Term Disability Insurance: Long-term disability insurance provides coverage for disabilities that extend for an extended period, often years or even until retirement age. It offers a more significant portion of the individual’s income.

Coverage: Disability insurance policies vary in terms of coverage. Some policies cover disabilities resulting from any cause, while others may only cover disabilities caused by accidents or injuries.

Benefit Amount: The benefit amount is the portion of the insured person’s income that the policy will replace in the event of a disability. It’s typically a percentage of their pre-disability income.

Waiting Period: Disability insurance policies often have a waiting period, also known as an elimination period, before benefits kick in. This waiting period can range from a few days to several months. The longer the waiting period, the lower the premium typically is.

Duration of Benefits: Policies also differ in how long they will pay benefits. Some policies provide benefits for a specific duration (e.g., 2 years), while others continue until the insured person reaches retirement age.

Premiums: Premiums for disability insurance depend on factors like age, health, occupation, and the extent of coverage. Generally, policies with higher benefit amounts and shorter waiting periods have higher premiums.

Definition of Disability: Policies may have different definitions of what constitutes a disability. Some may require that the insured person is unable to perform their specific occupation, while others may consider them disabled if they cannot perform any gainful work.

Optional Riders: Some disability insurance policies offer optional riders that can enhance coverage. For example, a cost-of-living adjustment (COLA) rider can increase benefit amounts over time to account for inflation.

Group vs. Individual Coverage: Disability insurance can be obtained through an employer as part of a group plan or purchased individually. Group plans often have more affordable premiums but may offer limited coverage.

Taxation: In some cases, disability insurance benefits may be taxable, depending on whether the premiums were paid with pre-tax or after-tax dollars. Tax regulations can vary, so it’s important to consult with a tax advisor.

Disability insurance is an important financial tool to protect against the potential loss of income due to a disability. It provides peace of mind and financial security for individuals and their families during challenging times when they are unable to work. It’s essential to carefully review policy terms, compare options, and choose coverage that aligns with your individual needs and circumstances.

Disability insurance in the United States provides financial protection for individuals who become unable to work due to a disability, whether it is temporary or permanent. This type of insurance is essential for ensuring financial stability during times when an individual’s ability to earn income is compromised.

Here are some key points to understand about disability insurance in the USA:

Types of Disability Insurance:

Short-Term Disability (STD): This type of insurance typically covers disabilities that last for a short period, often up to six months. It provides a percentage of your salary as replacement income.

Long-Term Disability (LTD): LTD insurance kicks in when a disability lasts for an extended period, potentially for several years or even until retirement age. It also provides a portion of your income.

Sources of Disability Insurance:

Employer-Sponsored Plans: Many employers offer disability insurance as part of their employee benefits package. This coverage can be either short-term, long-term, or both.

Social Security Disability Insurance (SSDI): This federal program provides financial assistance to individuals with disabilities who meet specific criteria, including having a severe and long-lasting disability.

Individual Policies: Some individuals purchase disability insurance policies independently to ensure coverage beyond what their employer offers.

Coverage and Benefits:

Disability insurance typically replaces a percentage of your income (often 50-70%) if you become disabled and cannot work.

The exact benefits and coverage terms vary depending on the policy and the insurance provider.

Policies may have waiting periods (known as the elimination period) before benefits start, often ranging from a few days to several months.

Some policies offer additional riders, such as cost-of-living adjustments (COLA) or partial disability benefits.

Eligibility and Qualification:

To qualify for disability benefits, you must meet the specific criteria outlined in your policy or, in the case of SSDI, the Social Security Administration’s guidelines.

Disability is generally defined as a medical condition that prevents you from performing your regular job duties.

Cost and Premiums:

The cost of disability insurance premiums depends on factors such as your age, health, occupation, and the amount of coverage you desire.

Employer-sponsored plans may offer more favorable rates, but individual policies can be customized to your needs.

Filing a Claim:

To receive disability benefits, you will need to file a claim with your insurance provider or the Social Security Administration.

Medical documentation and evidence of your disability are typically required.

Duration of Benefits:

Benefits can vary in duration, depending on the policy. Short-term disability benefits are typically paid for a few months, while long-term disability benefits can last for years or until retirement age.

Tax Implications:

The taxation of disability benefits depends on how the insurance premiums were paid. Benefits from employer-sponsored plans are often subject to income tax, while those from individual policies may be tax-free.

Appeals and Legal Assistance:

If your disability claim is denied, you have the right to appeal the decision. Legal assistance may be necessary in some cases to navigate the appeals process.

Consideration and Planning:

Disability insurance is an important aspect of financial planning, as it provides a safety net in case of unexpected health issues or accidents.

When choosing a policy, carefully review the terms, coverage limits, and premiums to ensure it meets your needs.

Coordination with Other Benefits:

If you have disability insurance through your employer, it’s important to understand how it coordinates with other benefits you may be eligible for, such as workers’ compensation or Social Security Disability Insurance (SSDI). In some cases, the benefits from these programs may offset or reduce your disability insurance payments.

Changing Jobs or Coverage:

If you change jobs, your disability insurance coverage may change or cease altogether. Be sure to understand your new employer’s benefits package and consider the option of purchasing individual coverage to bridge any gaps.

Pre-Existing Conditions:

Some disability insurance policies may have exclusions or waiting periods for pre-existing conditions. It’s crucial to be aware of these limitations and how they could affect your coverage.

Regular Review of Coverage:

Your financial situation and needs can change over time. It’s advisable to regularly review your disability insurance coverage to ensure it aligns with your current circumstances.

Return-to-Work Programs:

Many disability insurance policies offer support for returning to work gradually, known as “return-to-work” or “rehabilitation” programs. These programs can help individuals transition back to their regular work duties after a disability.

Communication with Healthcare Providers:

Maintain open communication with your healthcare providers regarding your disability and recovery progress. Their documentation and support can be critical when filing a disability insurance claim.

Education and Information:

Being well-informed about the terms of your disability insurance policy is essential. Read your policy documents carefully, and don’t hesitate to ask your employer’s HR department or insurance provider for clarification on any points of confusion.

Financial Planning Beyond Disability Insurance:

While disability insurance provides valuable protection, it’s just one aspect of financial planning. Consider other financial tools such as emergency funds, retirement savings, and investments to build a comprehensive financial safety net.

Seeking Legal Assistance:

If you encounter challenges with your disability insurance claim, legal assistance from an attorney experienced in disability insurance claims can be beneficial. They can help navigate complex disputes and ensure you receive the benefits you are entitled to.

Peace of Mind:

Disability insurance is designed to provide peace of mind during difficult times. Knowing that you have a financial safety net in place can reduce stress and allow you to focus on your recovery and well-being.

In conclusion, disability insurance is a critical component of financial planning, offering financial protection in the event of a disabling illness or injury. Understanding the details of your policy, staying informed about your rights and options, and seeking professional advice when needed are all essential steps in ensuring that you are adequately protected in the face of unexpected disability.

Group vs. Individual Disability Insurance:

Group disability insurance, provided by employers, often offers more affordable rates due to group buying power. However, it may have limitations on coverage and may not be portable if you change jobs. Individual disability insurance, on the other hand, provides more control over coverage, but it can be more expensive.

Understanding Own-Occupation vs. Any-Occupation Policies:

Disability insurance policies can be classified as either own-occupation or any-occupation. Own-occupation policies provide benefits if you can’t perform the specific job you were doing when you became disabled. Any-occupation policies only pay benefits if you can’t work in any job for which you are reasonably qualified. Own-occupation policies are generally considered more favorable because they provide broader coverage.

Regularly Update Your Information:

Make sure that your insurance provider has up-to-date contact information, including changes in address and phone number, to ensure that you can be reached in case of a disability claim.

Non-Cancellable vs. Guaranteed Renewable Policies:

Non-cancellable policies provide a higher level of protection because the insurance company cannot increase your premiums or change the terms as long as you pay your premiums on time. Guaranteed renewable policies ensure your right to renew the policy but may allow the insurer to adjust premiums for a broader group of policyholders.

Consider Additional Riders:

Depending on your specific needs, consider adding riders to your disability insurance policy. Riders can enhance your coverage by offering options such as future purchase options, catastrophic disability benefits, or residual disability benefits.

Consultation with Financial Advisors:

Disability insurance is just one element of your overall financial plan. Consult with a financial advisor to ensure that your insurance coverage aligns with your broader financial goals and strategies.

Maintain Good Health:

While disability insurance is essential, it’s equally important to take care of your health. Maintaining a healthy lifestyle can reduce the risk of disability and improve your overall well-being.

Family Considerations:

If you have dependents, your disability can affect not only your income but also your family’s financial stability. Adequate coverage can help protect your loved ones during challenging times.

Documentation and Record-Keeping:

Keep copies of all insurance-related documents, correspondence, and medical records. This can be invaluable in case you need to file a claim or provide evidence of your disability.

Review and Adjust as Needed:

Life circumstances change, so it’s important to periodically review and adjust your disability insurance coverage to ensure that it remains sufficient and appropriate for your situation.

Consider the Waiting Period Carefully:

When selecting a disability insurance policy, pay close attention to the waiting period, also known as the elimination period. This is the period of time you must wait after becoming disabled before benefits start. Longer waiting periods typically result in lower premiums, but they can leave you without income for a more extended period.

Know Your State’s Laws:

Some states have specific regulations regarding disability insurance, including minimum benefit requirements and consumer protections. Familiarize yourself with your state’s laws to ensure that your coverage complies with local regulations.

Understand Cost-of-Living Adjustments (COLA):

Some disability insurance policies offer COLA riders, which adjust your benefits over time to keep pace with inflation. This can be especially important for maintaining your purchasing power during a long-term disability.

Emergency Fund as Complement:

While disability insurance is crucial, having an emergency fund is also essential. An emergency fund can cover immediate expenses and bridge the gap between the start of a disability and when insurance benefits kick in.

Review Your Coverage After Major Life Events:

Major life changes such as marriage, the birth of a child, or a significant increase in income should prompt a review of your disability insurance coverage. You may need to adjust your coverage to reflect your changing circumstances.

Maintain a Strong Support Network:

A strong support network of family and friends can be invaluable during a period of disability. They can provide emotional support and assistance with daily tasks, which can aid in your recovery.

Consider Long-Term Care Insurance:

Long-term care insurance is distinct from disability insurance and covers the costs of care associated with aging or chronic illnesses. It’s worth considering this type of insurance as part of your overall financial planning.

Regularly Update Beneficiaries:

If your disability insurance policy includes death benefits, make sure your designated beneficiaries are up to date. Life changes such as marriages, divorces, or the birth of children may necessitate beneficiary updates.

Take Advantage of Employer-Sponsored Benefits:

If your employer offers disability insurance as part of your benefits package, take advantage of it. It can often provide more affordable coverage compared to individual policies.

Consult a Financial Planner:

For a comprehensive financial strategy, consider consulting with a certified financial planner. They can help you assess your overall financial health and integrate disability insurance into a broader plan for your financial future.