Introduction

Auto and home insurance are essential financial tools Auto And Home Insurance Companies in USA that provide peace of mind and financial security in case of unexpected events. While these insurance types share similarities, they also have distinct features and providers. Auto And Home Insurance Companies in USA In this article, we will explore the top auto and home insurance companies in the USA and help you make an informed choice.

Understanding Auto Insurance

Types of Coverage Auto And Home Insurance Companies in USA

Auto insurance typically offers various types of coverage, including:

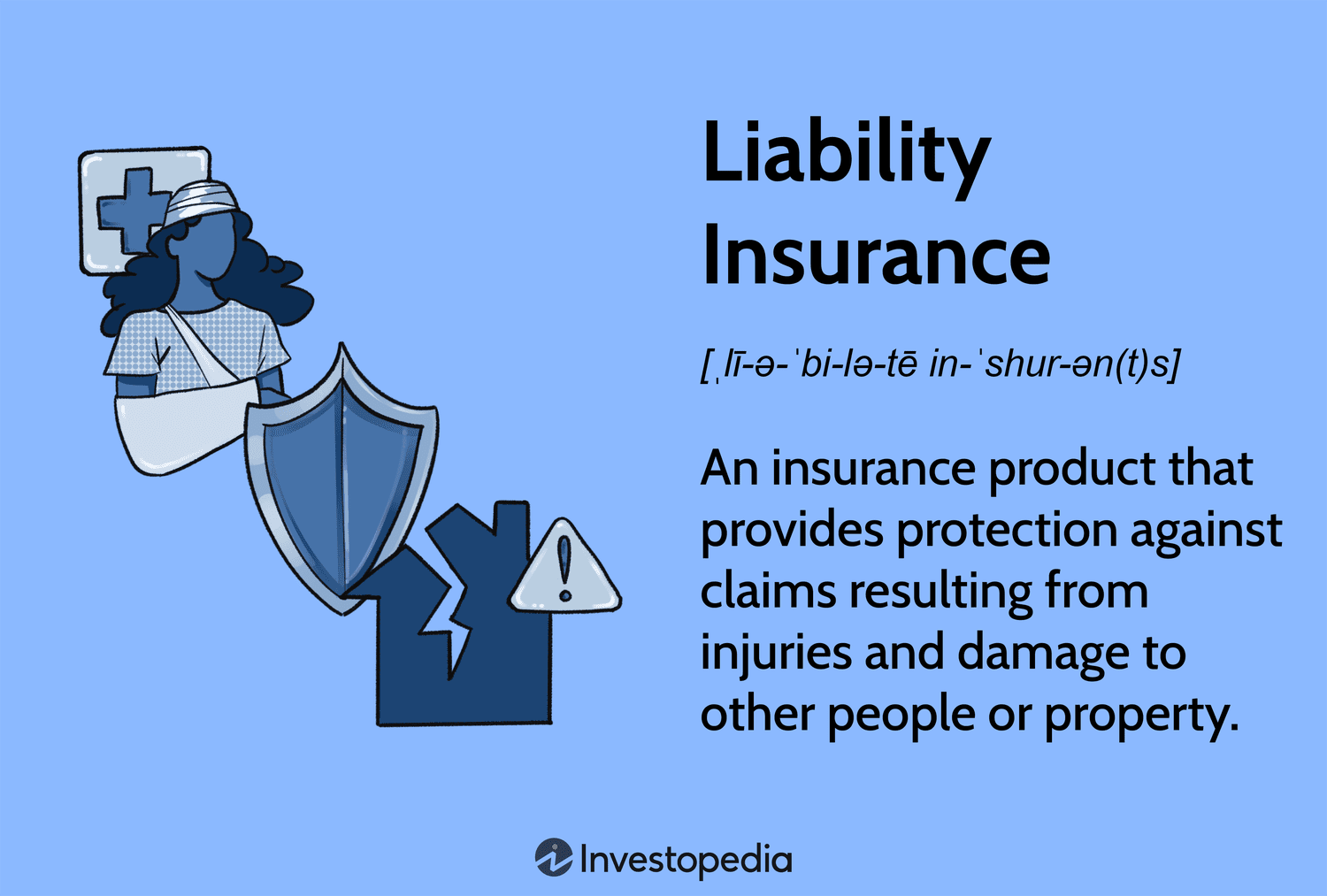

Liability Coverage

Collision Coverage

Comprehensive Coverage

Uninsured/Underinsured Motorist Coverage

Personal Injury Protection (PIP)

Each type of coverage serves a unique purpose and may be required or optional depending on your state’s regulations and your personal preferences.

Factors Affecting Auto Insurance Rates

When determining your auto insurance rates, Auto And Home Insurance Companies in USA providers consider factors such as:

Your Driving Record

Vehicle Type

Location

Age and Gender

Credit Score

Understanding how these factors affect your rates can help you find the most affordable coverage.

Top Auto Insurance Companies

Company A

Company A has consistently ranked Auto And Home Insurance Companies in USA among the top auto insurance providers in the USA. They are known for their competitive rates and excellent customer service. With a wide range of coverage options, they cater to drivers of all backgrounds.

Company B

Company B prides itself on its flexibility. They offer customizable policies that allow you to tailor your coverage to your specific needs. Whether you’re a young driver or a seasoned pro, Company B has options for you.

Company C

Company C is renowned for its discounts and rewards programs. They offer incentives for safe driving and loyalty, making them an attractive choice for those looking to save on auto insurance.

Evaluating Home Insurance

Types of Coverage

Home insurance, Auto And Home Insurance Companies in USA like auto insurance, offers several types of coverage, including:

Dwelling Coverage

Personal Property Coverage

Liability Coverage

Additional Living Expenses

These coverage types ensure your home and belongings are protected in various situations.

Factors Affecting Home Insurance Rates

Factors influencing home insurance rates include:

Location and Crime Rates

Home Age and Condition

Coverage Limits

Deductible Amount

Understanding these factors helps you choose the right home insurance policy.

Top Home Insurance Companies

Company X

Company X is known for its comprehensive home insurance policies. They offer coverage for a wide range of perils and ensure that your home is protected in even the most challenging circumstances.

Company Y

Company Y specializes in catering to first-time homeowners. They offer affordable rates and guidance to help new homeowners navigate the complexities of home insurance.

Company Z

Company Z stands out for its exceptional customer service. They provide 24/7 support and swift claims processing, ensuring that homeowners have peace of mind.

Combining Auto and Home Insurance

Many insurance companies offer discounts for bundling auto and home insurance policies. This can lead to substantial savings and the convenience of dealing with a single insurer for both your car and home.

Choosing the Right Insurance Company

When selecting an insurance company, consider the following factors:

Customer Reviews and Ratings

Reading reviews and checking ratings from current customers can give you insight into the company’s reputation and service quality.

Financial Strength

Ensure that the company has the financial strength to fulfill its obligations in case of claims.

Customization Options

Look for insurers that allow you to tailor your coverage to your unique needs.

The Importance of Regular Policy Reviews

Insurance is not a one-size-fits-all solution. Your circumstances and needs may change over time. Therefore, it’s crucial to review your policies regularly, ideally at least once a year. Here’s why:

Life Changes: Major life events, such as getting married, having children, or buying a new home, can significantly impact your insurance needs. For instance, you may require more coverage to protect your growing family or your new property.

Market Changes: The insurance market can fluctuate, affecting rates and coverage options. Periodic reviews ensure you stay informed about any changes in the industry that might benefit or affect your coverage.

Discount Opportunities: Over time, insurers may introduce new discounts or rewards programs. Regular reviews help you take advantage of these opportunities to save on your premiums.

Coverage Gaps: As your life evolves, so do your risks. An annual review allows you to identify and address any coverage gaps that may have emerged since you initially purchased your policies.

Understanding Deductibles

When selecting an insurance policy, whether it’s for your car or home, you’ll encounter the term “deductible.” This is the amount you’ll be responsible for paying out of pocket before your insurance coverage kicks in.

For example, if you have a car insurance policy with a $500 deductible and you’re in an accident that causes $2,000 in damages, you’ll need to pay the first $500, and your insurance provider will cover the remaining $1,500.

Choosing the right deductible amount is essential. A higher deductible typically results in lower premiums, but it also means you’ll have more upfront costs in the event of a claim. On the other hand, a lower deductible means higher premiums but less out-of-pocket expense when you need to make a claim.

Consider your financial situation and risk tolerance when deciding on a deductible. If you have significant savings and can comfortably handle a higher deductible, it might be a cost-effective choice. However, if you prefer to minimize immediate expenses after a claim, a lower deductible may be more suitable.

The Claims Process

Understanding how the claims process works is vital because it’s when you’ll rely on your insurance the most. Here’s a general overview:

Report the Incident: Whether it’s a car accident, home burglary, or other covered event, contact your insurance provider promptly. They will guide you on the next steps.

Documentation: Provide all necessary documentation, such as a police report for accidents or a list of stolen items for home insurance claims. The more information you can provide, the smoother the process.

Assessment: An adjuster will assess the damage or loss to determine the validity of the claim. They may also estimate the cost of repairs or replacement.

Resolution: Once your claim is approved, your insurance company will provide compensation according to the terms of your policy. This could be a check for repairs or a reimbursement for expenses.

Resolution Disputes: If there are disputes regarding your claim, work with your insurance company to resolve them. Most disputes can be settled through negotiation or mediation.

Appeals: If you believe your claim was unfairly denied or you’re unsatisfied with the resolution, you can appeal the decision through your insurance provider’s established process.

Remember, maintaining open communication with your insurer is key to a smooth claims experience.

Making Informed Choices

As a consumer, you have the power to make informed choices when it comes to your insurance. Take advantage of online resources, customer reviews, and expert opinions to assess insurance companies thoroughly. Additionally, consider seeking advice from insurance agents who can provide personalized recommendations based on your unique circumstances.

In conclusion, auto and home insurance are essential safeguards for your assets and financial well-being. By understanding the types of coverage, factors affecting rates, and the top companies in the USA, you can make informed decisions to protect what matters most. Regular policy reviews, understanding deductibles, and being familiar with the claims process empower you to navigate the complex world of insurance with confidence. So, take the time to assess your needs, compare options, and ensure you have the right coverage to secure your future.

Discounts and Savings Strategies

Insurance companies often offer various discounts and strategies to help policyholders save money while maintaining adequate coverage. Here are some common ways to reduce your insurance costs:

Multi-Policy Discounts

As mentioned earlier, bundling your auto and home insurance with the same company can lead to substantial savings. This is often referred to as a multi-policy or multi-line discount. By consolidating your coverage, you not only save money but also simplify your insurance management.

Safe Driving Discounts

Many auto insurance providers reward safe drivers with discounts. If you have a clean driving record without accidents or traffic violations, you’re likely to qualify for these discounts. Some insurers even offer usage-based insurance, where your premiums are based on your actual driving habits.

Home Safety Features

Installing safety features in your home, such as smoke detectors, security systems, and impact-resistant roofing, can qualify you for discounts on your home insurance premiums. These measures reduce the risk of damage or loss, which is advantageous for both you and your insurer.

Good Student Discounts

If you’re a student with good grades, you may be eligible for discounts on your auto insurance. Insurers often reward responsible academic performance as an indicator of responsible behavior on the road.

Loyalty Discounts

Staying with the same insurance company for an extended period can sometimes result in loyalty discounts. These rewards typically increase the longer you remain a policyholder, providing an incentive for customer loyalty.

Pay-in-Full Discounts

Paying your insurance premium annually or semi-annually instead of monthly can save you money. Insurance companies may offer discounts for policyholders who choose to pay their premiums in full upfront.

Navigating Complex Insurance Jargon

Insurance contracts can be riddled with complex terms and jargon that may seem intimidating. However, understanding some key terms can make the process less daunting:

Premium: This is the amount you pay to the insurance company in exchange for coverage. Premiums can vary based on factors like coverage type, deductible, and your personal information.

Coverage Limit: The maximum amount your insurance company will pay for a covered loss. For instance, if your home insurance policy has a $200,000 coverage limit for dwelling coverage, that’s the most the insurer will pay for covered damages to your home.

Exclusion: These are specific situations or events that your insurance policy doesn’t cover. It’s essential to understand what your policy excludes to avoid surprises during a claim.

Policyholder: You, the person who holds the insurance policy and is entitled to its benefits.

Rider: Also known as an endorsement, a rider is an addition to your insurance policy that provides extra coverage for specific items or situations. For example, you might add a rider to cover valuable jewelry.

Underwriting: The process insurance companies use to evaluate your risk and determine your premium. It involves analyzing factors like your age, location, and claims history.

Claim: A formal request made to your insurance company to cover a loss or damage that is covered by your policy.

Understanding these terms can empower you when discussing your insurance needs with agents and comparing policies.

Staying Informed for Future Security

Lastly, staying informed about changes in your life and your insurance policies is essential for long-term financial security. Life events such as marriage, the birth of a child, or purchasing a new vehicle can all impact your insurance needs. As your circumstances evolve, it’s vital to update your policies accordingly to ensure that you have adequate coverage.

Moreover, regularly reviewing your policies, shopping around for better rates, and staying informed about changes in the insurance industry can help you make the most of your insurance investments.

The Role of Credit Scores

In the realm of insurance, credit scores play a significant role, especially in determining your auto insurance premiums. Many insurance companies use credit-based insurance scores to assess risk. Here’s how it works:

Insurance providers use statistical models that analyze your credit history to predict your likelihood of filing a claim. While this practice may seem unrelated to insurance, studies have shown a correlation between credit history and the likelihood of filing a claim. People with better credit scores tend to have fewer claims, and thus, they are often rewarded with lower premiums.

To maintain or improve your credit-based insurance score:

Pay bills on time.

Reduce outstanding debt.

Monitor your credit report for errors.

Avoid opening unnecessary new credit accounts.

By managing your credit responsibly, you can potentially lower your auto insurance premiums.

Filing Claims: Dos and Don’ts

When it comes to filing insurance claims, following best practices can help ensure a smooth process and fair compensation:

Dos

Contact Your Insurer Promptly: Notify your insurance company as soon as an incident occurs. Most policies require you to report accidents or losses within a certain timeframe.

Document the Incident: Gather as much evidence as possible, such as photos, witness statements, and police reports, to support your claim.

Be Accurate: Provide accurate information when reporting the incident. Misrepresenting facts can lead to claim denials.

Keep Records: Maintain records of all communication with your insurance company, including dates, times, and names of representatives.

Follow Instructions: Cooperate with your insurer’s requests, such as providing documentation or meeting with adjusters.

Don’ts

Exaggerate or Fabricate: Never exaggerate or fabricate details of the incident. This can lead to insurance fraud and serious legal consequences.

Delay Reporting: Avoid delaying the reporting of an incident. Timely reporting is crucial for processing your claim.

Admit Fault: Refrain from admitting fault at the scene of an accident, especially if you’re unsure. Fault is determined during the claims process.

Settle Too Quickly: Avoid accepting a settlement offer from another party’s insurer without consulting your own insurance company first. Their offer may not fully cover your expenses.

Ignore Denials: If your claim is denied, don’t give up. You have the right to appeal or seek legal advice to resolve disputes.

Managing Your Premiums

While understanding discounts is important, there are additional strategies for managing your insurance premiums effectively:

Shop Around: Don’t settle for the first quote you receive. Different insurers may offer varying rates and discounts, so it’s worth comparing options.

Maintain a Good Driving Record: Safe driving not only keeps you safe but also helps maintain a clean record, which can lead to lower premiums.

Review Your Coverage: Periodically review your coverage needs. As your circumstances change, you may need more or less coverage, which can impact your premiums.

Consider Higher Deductibles: If you have a solid emergency fund, raising your deductibles can reduce your premiums. Just be prepared for higher out-of-pocket expenses in case of a claim.

Managing Your Home Insurance Costs

Home insurance is a critical safeguard for homeowners, but it’s essential to manage its costs effectively. Here are some tips to help you do just that:

Home Security Measures

Investing in security measures can not only protect your home but also lead to reduced home insurance premiums. Installing features like deadbolt locks, burglar alarms, and security cameras can deter potential thieves and lower your insurance costs.

Fire Prevention

Home fires can result in devastating losses. To mitigate this risk, consider installing smoke detectors, fire extinguishers, and fire-resistant roofing materials. These safety measures can lead to lower premiums.

Home Renovations

Home improvements can impact your insurance premiums. Upgrading your plumbing, electrical systems, or the roof can make your home less susceptible to damage and result in lower insurance costs.

Bundle with Auto Insurance

As mentioned earlier, bundling your auto and home insurance policies with the same insurer can lead to substantial discounts. This not only simplifies your insurance management but also saves you money.

The Role of Agents

Insurance agents can be invaluable resources when navigating the complex world of insurance. Here’s how they can assist you:

Expert Guidance: Agents are knowledgeable about the insurance industry and can help you understand policy options, coverage limits, and endorsements.

Customized Advice: They can provide personalized recommendations based on your specific needs and circumstances. This ensures you get coverage tailored to you.

Claims Assistance: In the event of a claim, agents can guide you through the process, helping you complete the necessary paperwork and liaising with the insurance company on your behalf.

Periodic Reviews: Agents can periodically review your policies to ensure they still meet your needs. This is especially helpful when major life changes occur.

Access to Multiple Insurers: Independent agents can offer policies from multiple insurance companies, allowing you to compare options and find the best coverage at the most competitive rates.

Insurance in Times of Natural Disasters

The United States is prone to natural disasters such as hurricanes, floods, wildfires, and tornadoes. Understanding how your insurance policies cover these events is crucial:

Flood Insurance: Standard homeowners’ policies typically do not cover flood damage. If you live in an area prone to flooding, consider purchasing a separate flood insurance policy through the National Flood Insurance Program (NFIP) or a private insurer.

Earthquake Insurance: Earthquake coverage is usually not included in standard policies. If you live in an earthquake-prone region, explore earthquake insurance options.

Hurricane and Windstorm Coverage: In coastal areas prone to hurricanes, insurers may impose separate deductibles for hurricane and windstorm damage. Review your policy to understand these deductibles.

Wildfire Insurance: If you live in an area susceptible to wildfires, ensure your home insurance includes coverage for fire damage. Some insurers may require additional endorsements for wildfire coverage.

Understanding your policy’s provisions for natural disasters and ensuring that you have adequate coverage is essential to protect your home and belongings in times of crisis.

Emerging Trends in Insurance

The insurance industry is constantly evolving to adapt to changing demographics, technology, and consumer expectations. Here are some emerging trends you should be aware of:

Telematics in Auto Insurance

Telematics, which involves using technology to monitor driving habits, is becoming increasingly popular in the auto insurance sector. Insurers provide policyholders with devices or mobile apps that track their driving behavior, including factors like speed, braking, and mileage. Safe drivers are often rewarded with lower premiums based on their actual driving habits.

Smart Home Devices

The rise of smart home devices, such as thermostats, security cameras, and water leak detectors, is influencing home insurance. Some insurers offer discounts to homeowners who install these devices, as they can help prevent or mitigate damage and loss.

Conclusion

Choosing the right auto and home insurance companies in the USA is a crucial decision that impacts your financial security and peace of mind. Evaluate your needs, compare quotes, and read reviews to make an informed choice.

FAQ

Can I save money by bundling auto and home insurance?

Yes, many insurance companies offer discounts for bundling policies, resulting in significant savings.

How do I determine the right coverage limits for my home insurance?

Consider factors like your home’s value, location, and personal assets when deciding on coverage limits.

What should I do after a car accident to ensure a smooth insurance claim process?

Contact your insurance company promptly, provide accurate information, and document the accident scene if possible.

Are there any discounts available for safe drivers?

Yes, several insurance companies offer discounts and rewards for safe driving habits.

How often should I review and update my insurance policies?

It’s advisable to review your policies annually or when significant life changes occur, such as buying a new home or getting married.