Introduction

Driving a car in the United States offers incredible freedom and convenience, American Auto Insurance but it also comes with responsibilities. One of the most crucial responsibilities is having adequate auto insurance coverage. In this comprehensive guide, we will delve into the world of American auto insurance. From understanding the basics to navigating complex coverage options, American Auto Insurance we’ll ensure you’re well-informed about protecting yourself on the road.

American Auto Insurance

Why Auto Insurance Matters

Auto insurance isn’t just another monthly expense; it’s your financial safety net when accidents happen. Here’s why it matters:

Legal Requirement

American Auto Insurance

In the U.S., auto insurance is mandatory in almost every state. Driving without it can lead to fines, license suspension, or even legal action.

Financial Protection

American Auto Insurance

Auto insurance covers repair costs for your vehicle and medical bills in the event of an accident, preventing financial catastrophe.

Peace of Mind

Knowing you’re protected provides peace of mind. You can drive without constantly worrying about “what if.”

Types of Auto Insurance

Auto insurance isn’t one-size-fits-all. There are several coverage types to choose from:

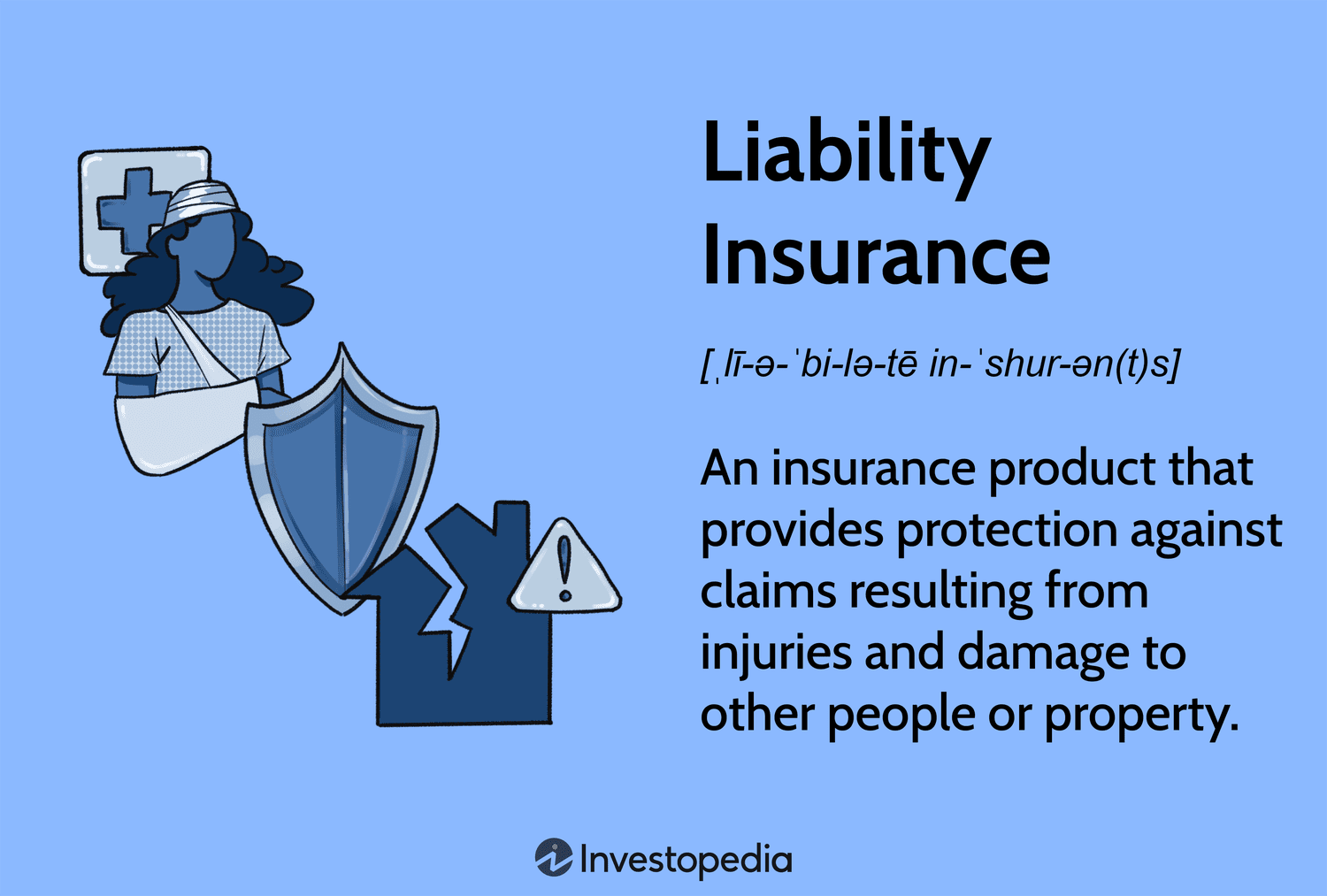

Liability Insurance (H3)

This covers injuries and property damage you cause to others in an accident. It’s usually the minimum required by law.

Collision Insurance

Collision insurance pays for damage to your vehicle in a crash, regardless of fault.

Comprehensive Insurance (H3)

Comprehensive coverage protects against non-collision incidents like theft, vandalism, or natural disasters.

Personal Injury Protection

PIP covers medical expenses for you and your passengers, no matter who’s at fault.

Factors Affecting Insurance Costs (H2)

Several factors influence how much you pay for auto insurance:

Driving Record

American Auto Insurance A clean driving record often results in lower premiums, while accidents and tickets can raise them.

Vehicle Type (H3)

The make and model of your car affect insurance rates. Sports cars may be more expensive to insure than sedans.

Location

Where you live matters. Urban areas often have higher insurance costs due to increased accident and theft rates.

Coverage Level

The more coverage you choose, the higher your premium will be. It’s essential to strike a balance between protection and cost.

Finding the Right Insurance Company

Not all insurance companies are equal. Here’s how to choose the right one for your needs:

Research (H3)

Read reviews, ask for recommendations, and compare quotes from different insurers.

Customer Service

Good customer service is crucial. You want a company that will assist you promptly when you need them.

Financial Stability (H3)

Check the financial strength rating of the insurance company to ensure they can meet their obligations.

Saving on Auto Insurance

Everyone wants to save on insurance premiums. Here’s how:

Bundle Policies (H3)

Consider bundling your auto insurance with other policies like home or renters insurance for discounts.

Defensive Driving Courses

Completing a defensive driving course can often lead to lower premiums.

Maintain a Good Credit Score (H3)

Your credit score can influence your insurance rates. Keeping it in good shape can save you money.

The Claims Process

Understanding how the claims process works is essential for making the most of your auto insurance. Here’s what you need to know:

Report Promptly

After an accident, it’s crucial to report the incident to your insurer as soon as possible. Delays can complicate the claims process.

Gather Information

Collect all relevant information, such as the other driver’s details, witnesses, and photos of the accident scene. This documentation will help with your claim.

Claims Adjuster

American Auto Insurance Your insurance company will assign a claims adjuster to your case. They will assess the damage, gather information, and determine the settlement.

Settlement (H3)

Once the investigation is complete, the insurer will offer a settlement. You can negotiate if you believe it’s insufficient.

Optional Coverage

In addition to standard auto insurance, you can opt for additional coverage to further protect yourself:

Uninsured/Underinsured Motorist Coverage (H3)

This coverage safeguards you if you’re in an accident with a driver who has insufficient or no insurance.

Rental Car Reimbursement

If your car is in the shop for repairs due to an accident, this coverage helps with the cost of a rental car.

Gap Insurance (H3)

If you’re financing or leasing a vehicle, gap insurance covers the difference between what you owe on the car and its actual value.

Teen Drivers

If you have a teenager who’s ready to hit the road, be prepared for the impact on your insurance:

Teen Driver Policies

Adding a teenager to your policy can be costly due to their lack of experience. Inquire about good student discounts or driver’s education courses to reduce premiums.

Responsible Driving Education

Teaching your teen safe and responsible driving habits not only ensures their safety but can also keep insurance costs down.

Monitoring Technology

Some insurance companies offer monitoring technology that tracks a teen’s driving behavior. Safe driving can result in lower premiums.

Additional Tips for Smart Insurance Shopping

When it comes to American auto insurance, being a savvy shopper can save you both money and hassle:

Regular Policy Reviews

Don’t let your auto insurance policy gather dust. Regularly review your coverage to ensure it still suits your needs. As your circumstances change, so should your coverage.

Compare Quotes

Shopping around is key to getting the best insurance rates. Obtain quotes from multiple providers, but remember that the cheapest option may not provide the best coverage.

Understand Deductibles

Deductibles are the out-of-pocket expenses you must pay before your insurance kicks in. Higher deductibles can lower your premium but increase your immediate costs in the event of a claim.

Avoid Lapses in Coverage

Maintain continuous coverage, even if you switch providers. Insurance companies view lapses in coverage as a risk factor, potentially leading to higher premiums.

Specialized Auto Insurance

Certain situations may require specialized auto insurance coverage:

Classic Car Insurance

If you own a classic or antique car, standard insurance may not provide sufficient coverage. Classic car insurance caters to the unique needs of these vehicles.

Commercial Auto Insurance

For business owners, personal auto insurance may not cover vehicles used for work purposes. Commercial auto insurance is designed to protect business vehicles.

SR-22 Insurance

If you’ve had legal issues related to driving, such as a DUI or multiple traffic violations, you may need SR-22 insurance to reinstate your driver’s license.

Staying Informed

Auto insurance is a dynamic industry. Stay informed about changes in regulations, new discounts, and emerging insurance technologies to make informed decisions.

Conclusion

American auto insurance is your ally on the open road, providing the financial protection and peace of mind you need while driving. Whether you’re a seasoned driver or a newcomer, understanding the nuances of auto insurance is vital for responsible car ownership.

By following the tips in this guide, you can make informed decisions, secure the right coverage for your needs, and navigate the complex world of auto insurance with confidence.

The Future of Auto Insurance

As technology advances, the landscape of auto insurance is evolving. Here’s a glimpse into the future:

Usage-Based Insurance (H3)

Insurance companies are increasingly offering usage-based policies. These policies monitor your driving habits through telematics devices or smartphone apps. Safer driving can lead to lower premiums.

Autonomous Vehicles

With the rise of autonomous vehicles, insurance may shift from personal to product liability. Understanding how insurance adapts to this new technology will be crucial for drivers.

AI and Predictive Analytics

Insurers are harnessing the power of artificial intelligence and predictive analytics to assess risk more accurately. This could lead to more personalized and affordable coverage.

Environmental Considerations (H2)

Environmental concerns are shaping the insurance industry in various ways:

Electric Vehicle Coverage

As electric vehicles become more prevalent, insurance policies may need to adapt to cover the unique risks associated with these cars, such as battery damage or charging accidents.

Climate Change Impact

With the increasing frequency of extreme weather events, insurance companies are reassessing how they handle claims related to climate change-related damages.

Insurance and Ride-Sharing

The rise of ride-sharing services like Uber and Lyft has created new insurance challenges:

Hybrid Coverage

Drivers who work for ride-sharing services often need hybrid insurance policies that provide coverage both while they’re driving for personal use and while they’re actively working.

Ride-Share Company Coverage

Ride-sharing companies typically offer insurance for their drivers, but it’s essential to understand the coverage limitations and when your personal insurance may be in effect.

Final Thoughts

American auto insurance is a complex but necessary aspect of owning and operating a vehicle in the United States. It’s more than just a legal requirement; it’s a financial safety net that protects you and others on the road.

To make the most of your auto insurance, stay informed about industry trends and regulations, regularly review your coverage, and shop around for the best rates. By doing so, you can ensure that you have the right coverage at the right price.

Certainly, here’s more information on American auto insurance:

Factors Affecting Premiums: Insurance companies use various factors to determine your premium rates, including your driving record, age, gender, marital status, location, the make and model of your vehicle, and even your credit score in some cases. Maintaining a clean driving record and improving your credit can often lead to lower premiums.

Certainly! Auto insurance is a type of insurance that provides financial protection in case of accidents, theft, or damage to a vehicle. Here are some key points about auto insurance:

Coverage Types:

Liability Insurance: This covers damages and injuries you may cause to others in an accident.

Collision Insurance: This pays for damages to your own vehicle caused by a collision, regardless of fault.

Comprehensive Insurance: It covers non-collision-related damages, such as theft, vandalism, or natural disasters.

Uninsured/Underinsured Motorist Coverage: This helps if you’re in an accident with a driver who doesn’t have insurance or has inadequate coverage.

Premiums: You pay regular premiums to the insurance company in exchange for coverage. Premiums can vary widely based on factors like your driving history, the type of car you drive, your location, and coverage choices.

Insurance Score: Your insurance score, based on factors like your credit history and driving record, can impact your insurance premium. Maintaining good credit and a clean driving record can help lower your rates.

Coverage Limits: It’s essential to understand the limits of your coverage. For example, if your liability coverage is $50,000/$100,000, it means your insurer will pay up to $50,000 per person and up to $100,000 per accident for bodily injuries you cause to others.

Ridesharing and Delivery Services: If you work for ridesharing companies like Uber or Lyft or deliver food with services like DoorDash, you may need special insurance coverage. Standard personal auto insurance might not cover commercial activities.

Lapses in Coverage: Letting your insurance coverage lapse, even for a short period, can result in higher premiums when you reinstate your policy. Continuous coverage is often rewarded with lower rates.

Accident Forgiveness: Some insurance companies offer accident forgiveness, which means your rates won’t increase after your first at-fault accident, as long as you have a clean driving record otherwise.

Policy Add-Ons: You can tailor your auto insurance policy to your needs by adding options like roadside assistance, custom equipment coverage (for vehicle modifications), and pet coverage (for vet bills if your pet is injured in an accident).

Premium Payment Options: Most insurers offer flexible payment plans. You can choose to pay your premium in full upfront or opt for monthly, quarterly, or semi-annual payments.

Discounts for Safe Driving: Some insurers offer usage-based insurance (UBI) programs where your rates are based on your actual driving habits. Installing a device that tracks your driving can result in discounts for safe driving.

No-Fault Insurance States: In some states, the “no-fault” system means each driver’s insurance pays for their injuries and damages, regardless of who caused the accident. These states often have unique auto insurance laws.

Annual Review: It’s a good practice to review your auto insurance policy annually to ensure it still meets your needs. Life changes, such as moving, getting married, or buying a new car, can affect your insurance requirements.

Legal Requirements: Driving without auto insurance in most states is illegal, and you can face severe penalties if caught. Ensure that you meet your state’s minimum coverage requirements.

Insurance Agents and Brokers: You can purchase auto insurance directly from insurance companies, through independent agents who represent multiple insurers, or through exclusive agents who work for a single insurance company. Each option has its advantages.

Cancellation Policies: Insurance companies can cancel your policy for various reasons, such as non-payment or misrepresentation. It’s important to understand your insurer’s cancellation policy and the steps to take to avoid it.

Remember that auto insurance is not only a legal requirement in most states but also a crucial financial safety net. It’s a means of protecting yourself, your passengers, and other drivers on the road in case of accidents or unexpected events. Be proactive in understanding your policy and keeping it up to date to ensure you have the coverage you need.

Auto insurance in the United States is a critical financial product that provides protection and coverage for individuals and their vehicles in the event of accidents, damage, or theft. Here are some key aspects of American auto insurance:

Types of Coverage:

This is mandatory in most states. It covers the cost of injuries and property damage that you may cause to others in an accident.

Collision Coverage: This pays for repairs to your vehicle if it’s damaged in an accident, regardless of fault.

Comprehensive Coverage: This covers damage to your vehicle from non-accident incidents such as theft, vandalism, or natural disasters.

Uninsured/Underinsured Motorist Coverage: Protects you if you’re involved in an accident with a driver who has little or no insurance.

State Requirements: Auto insurance requirements vary by state. Each state has its own minimum liability coverage limits that drivers must meet. It’s essential to understand your state’s specific requirements.

Premiums: The cost of auto insurance, known as premiums, depends on various factors, including your driving history, the type of coverage you choose, your age, gender, location, and the make and model of your vehicle.

Deductibles: When you file a claim, you’ll need to pay a deductible before your insurance kicks in. Higher deductibles typically result in lower premiums, but you’ll pay more out of pocket if you have a claim.

Discounts: Many insurance companies offer discounts for factors such as safe driving records, bundling multiple policies (e.g., auto and home insurance), and anti-theft devices installed in your vehicle.

Policy Terms: Auto insurance policies typically last for six months or a year. At the end of the term, you can renew your policy or shop around for a new one.

Claims Process: If you’re in an accident or need to make a claim, you’ll contact your insurance company. They will assess the damage, determine fault, and provide compensation based on your policy terms.

Penalties for Non-Compliance: Driving without insurance or allowing your coverage to lapse can result in fines, license suspension, and other legal consequences, depending on your state’s laws.

Optional Coverage: In addition to the basic types of coverage, you can opt for extras like rental car coverage, roadside assistance, and gap insurance (covers the difference between your vehicle’s value and what you owe on a loan or lease).

Shopping for Insurance: It’s advisable to shop around and compare quotes from different insurance companies to find the best coverage and rates for your needs.

Teen Drivers: Insuring teenage drivers can be expensive due to their lack of experience. However, some companies offer discounts for good grades and driver’s education courses.

SR-22: If you’ve had a serious driving offense, like a DUI, your state may require you to obtain an SR-22 certificate as proof of financial responsibility before you can get your driver’s license reinstated.

Auto insurance is a crucial aspect of responsible vehicle ownership in the United States. It provides financial protection and peace of mind in the event of unexpected accidents or incidents on the road. Be sure to carefully review your policy and understand your coverage to ensure you have the protection you need.

Deductibles: This is the amount you pay out of pocket before your insurance coverage kicks in. Higher deductibles usually result in lower premiums.

Policy Limits: Every insurance policy has limits on how much it will pay out for different types of claims. You can choose these limits when you purchase your policy.

State Requirements: Auto insurance requirements vary by state and country. Most places require at least liability insurance.

Optional Coverage: In addition to the basic coverages, you can often add extra protection, such as rental car reimbursement, roadside assistance, or gap insurance.

Claim Process: When you’re in an accident or experience damage, you’ll need to file a claim with your insurance company. They will assess the damage, and if it’s covered, they will pay for the repairs or replacement based on your policy terms.

No-Fault Insurance: In some states, a “no-fault” system is in place. This means that each driver’s insurance pays for their own medical expenses and damages, regardless of who is at fault.

Discounts: Insurance companies often offer discounts for safe driving records, multiple policies (e.g., bundling auto and home insurance), and other factors.

Cancellation: Insurance companies can cancel your policy for various reasons, such as non-payment or a high number of claims. You can also choose to switch to a different insurer if you find a better deal.

It’s essential to understand your auto insurance policy thoroughly and choose coverage that suits your needs and budget. Auto insurance provides valuable protection and financial peace of mind in case of unexpected events on the road.

Optional Coverages: In addition to the standard coverages mentioned earlier, you can purchase optional coverages to enhance your protection. These may include rental car reimbursement, roadside assistance, and gap insurance (which covers the difference between the actual cash value of your car and the amount you owe on a loan or lease).

Payment Options: Most insurance companies offer flexible payment options. You can typically choose to pay your premium annually, semi-annually, quarterly, or monthly. Keep in mind that paying annually or semi-annually often results in cost savings, as there may be fewer administrative fees.

No-Fault Insurance: Some states have “no-fault” insurance systems, where each driver’s insurance company pays for their injuries and damages, regardless of who was at fault in an accident. This system is designed to expedite claims processing and reduce litigation.

Proof of Insurance: You’re usually required to carry proof of insurance in your vehicle at all times. This can be in the form of a physical insurance card or, in many cases, an electronic version on your smartphone. Law enforcement may request to see this proof during traffic stops.

Bundle and Save: Many insurance companies offer discounts when you bundle multiple insurance policies, such as auto and home insurance. This can result in significant savings on your premiums.

Teenage Drivers: If you have teenage drivers in your household, adding them to your policy can significantly increase your premiums due to their lack of driving experience. However, you can often qualify for discounts by enrolling them in driver’s education programs or maintaining good grades.

Lapses in Coverage: Allowing your insurance coverage to lapse by not paying your premiums can result in higher rates when you reinstate coverage, as insurers may view you as a higher risk.

Shop Around Annually: It’s a good practice to review your auto insurance policy and shop around for quotes annually. As your circumstances change and you accumulate a better driving record, you may find better deals with other insurers.

Usage-Based Insurance: Some insurance companies offer usage-based insurance programs that monitor your driving habits through a device or smartphone app. Safe driving behaviors can lead to discounts on your premiums.

Remember that auto insurance is a dynamic aspect of your financial life. Your needs may change over time, so it’s essential to regularly evaluate your coverage and consider adjustments as necessary to ensure you have the protection you need at a cost that fits your budget. Always consult with insurance professionals to get personalized advice based on your unique circumstances.

Auto insurance is a crucial requirement for drivers in the United States. It serves to protect both the driver and other parties involved in an accident. Here are some key points about American auto insurance:

Types of Coverage: American auto insurance typically offers several types of coverage, including:

Liability Coverage: This covers the cost of damage you may cause to someone else’s property or injuries to other people in an accident where you are at fault.

Collision Coverage: This pays for damage to your own vehicle in a collision with another vehicle or object.

Comprehensive Coverage: This covers non-collision-related damage to your vehicle, such as theft, vandalism, or damage from natural disasters.

Uninsured/Underinsured Motorist Coverage: This protects you if you’re involved in an accident with a driver who doesn’t have insurance or doesn’t have enough coverage.

Minimum Coverage Requirements: Each state in the U.S. has its own minimum insurance requirements that drivers must meet. These requirements vary, so it’s essential to understand what is mandated in your specific state.

Premiums: The cost of auto insurance premiums can vary widely based on factors such as your driving history, the type of car you drive, your age, and your location. Drivers with a history of accidents or traffic violations typically pay higher premiums.

Deductibles: When you file a claim, you’ll often have to pay a deductible before your insurance coverage kicks in. Higher deductibles usually result in lower premiums, but you’ll need to pay more out of pocket in the event of a claim.

Discounts: Many insurance companies offer discounts for safe driving, bundling policies (such as auto and home insurance), and other factors like being a good student or having anti-theft devices in your vehicle.

SR-22 Insurance: Some drivers may be required to obtain an SR-22 certificate, which is a form that proves you have the necessary insurance coverage. This is often mandated for individuals with serious traffic violations or DUI convictions.

Claims Process: If you’re in an accident or experience damage covered by your policy, you’ll need to file a claim with your insurance company. The process typically involves providing details about the incident, including photos and estimates for repairs.

Penalties for Driving Without Insurance: Driving without insurance is illegal in most states. Penalties can include fines, license suspension, and even vehicle impoundment.

Shopping for Insurance: It’s essential to shop around and compare quotes from different insurance companies to find the best coverage and rates for your needs.

Insurance Companies: There are many auto insurance companies in the United States, both national and regional. Some well-known national companies include State Farm, Geico, Progressive, and Allstate, among others.

Remember that auto insurance is a critical aspect of responsible car ownership in the United States. It not only provides financial protection but also ensures compliance with legal requirements. It’s crucial to understand your policy, its coverage, and your state’s requirements to make informed decisions about your auto insurance needs.

Ertainly, here’s more information about American auto insurance:

Claims Settlement: When you file a claim, your insurance company will investigate and determine the appropriate compensation based on the terms of your policy and the circumstances of the incident. They may pay for repairs directly to a repair shop or provide you with a check for the estimated repair costs.

Rental Car Coverage: Some insurance policies include rental car coverage, which can help cover the cost of a rental vehicle while your car is being repaired after an accident. This coverage can be invaluable to ensure you have transportation in case of a covered loss.

Accident Forgiveness: Some insurance companies offer accident forgiveness programs, which means your rates won’t increase after your first at-fault accident. This can be a valuable feature for maintaining affordable premiums over the long term.

Telematics and Usage-Based Insurance: Many insurance companies now offer telematics programs that use devices or smartphone apps to monitor your driving behavior. Safe driving habits can result in discounts or lower premiums. This type of insurance is particularly popular with younger drivers.

SR-22 and FR-44: In some cases, individuals who have had serious driving violations or DUI convictions may be required to file an SR-22 or FR-44 form with their state’s Department of Motor Vehicles (DMV). These forms are certificates of financial responsibility that prove you have the required insurance coverage.

Coverage While Traveling: Your auto insurance coverage often extends beyond your state’s borders, so you’re generally covered when driving in other parts of the United States. However, if you plan to travel internationally, you may need to purchase additional coverage or check if your existing policy offers international coverage.

Usage Restrictions: Some policies have usage restrictions, such as limitations on how far you can drive your vehicle or restrictions on using your car for ridesharing services like Uber or Lyft. It’s important to understand and adhere to these restrictions to avoid potential coverage gaps.

High-Risk Insurance: If you have a history of accidents or violations, it can be more challenging to find affordable insurance. In such cases, you may need to seek coverage from specialized high-risk insurance providers.

Policy Renewal: Your auto insurance policy typically renews automatically, but it’s essential to review the renewal terms each year. Rates can change, and you may want to adjust your coverage or shop around for better deals.

Customer Service: Good customer service is crucial when choosing an insurance company. You want a company that is responsive to your questions and concerns and handles claims efficiently.

Remember that auto insurance is not a one-size-fits-all product. Your needs, circumstances, and preferences may be unique, so it’s important to thoroughly research and compare insurance options to find the right coverage at the best price. Additionally, understanding the terms and conditions of your policy is essential to make sure you have adequate protection in case of an accident or other covered events.

Conclusion

American auto insurance is a vital aspect of responsible car ownership. It provides financial protection, legal compliance, and peace of mind. By understanding the types of insurance, factors affecting costs, and how to choose the right insurer, you can make informed decisions to safeguard your adventures on the road.

FAQ

What happens if I drive without insurance in the U.S.?

Driving without insurance can lead to fines, license suspension, and even legal action. It’s a serious offense in most states.

Is auto insurance mandatory in every state?

Auto insurance is mandatory in almost every state, but the requirements may vary. It’s crucial to understand the specific laws in your state.

How can I lower my auto insurance premiums?

You can lower your premiums by bundling policies, taking defensive driving courses, and maintaining a good credit score.

What does collision insurance cover?

Collision insurance covers the cost of repairing or replacing your vehicle after a collision, regardless of fault.

Do I need comprehensive insurance if I have collision coverage?

While collision insurance covers accidents, comprehensive insurance covers non-collision incidents like theft and natural disasters. Depending on your needs, both may be necessary for full protection.