Introduction

In the dynamic world of entrepreneurship, 10 Million Dollar Business Insurance Policy success and risk often go hand in hand. Every successful business owner understands the importance of safeguarding their hard-earned accomplishments. That’s where a Million Dollar Business Insurance Policy comes into play. In this comprehensive guide, we will explore what this insurance policy entails, 10 Million Dollar Business Insurance Policy why it is crucial for your business, and how to obtain one.

The Foundation: What is a Million Dollar Business Insurance Policy?

Understanding the Basics

10 Million Dollar Business Insurance Policy

Before delving into the intricacies of this policy, 10 Million Dollar Business Insurance Policy let’s establish a clear understanding of its core concept. A Million Dollar Business Insurance Policy is a robust insurance plan designed to protect businesses with assets and revenues in the million-dollar range. It acts as a safety net, shielding your company from unforeseen circumstances that could threaten its financial stability.

The Importance of a Million Dollar Business Insurance Policy

10 Million Dollar Business Insurance Policy

Protecting Your Assets 10 Million Dollar Business Insurance Policy

One of the primary reasons to invest in this policy is to safeguard your business assets. In a world where accidents, natural disasters, and unforeseen legal challenges can strike at any moment, having a substantial insurance policy becomes imperative. It ensures that your company’s physical assets, such as buildings and equipment, are protected.

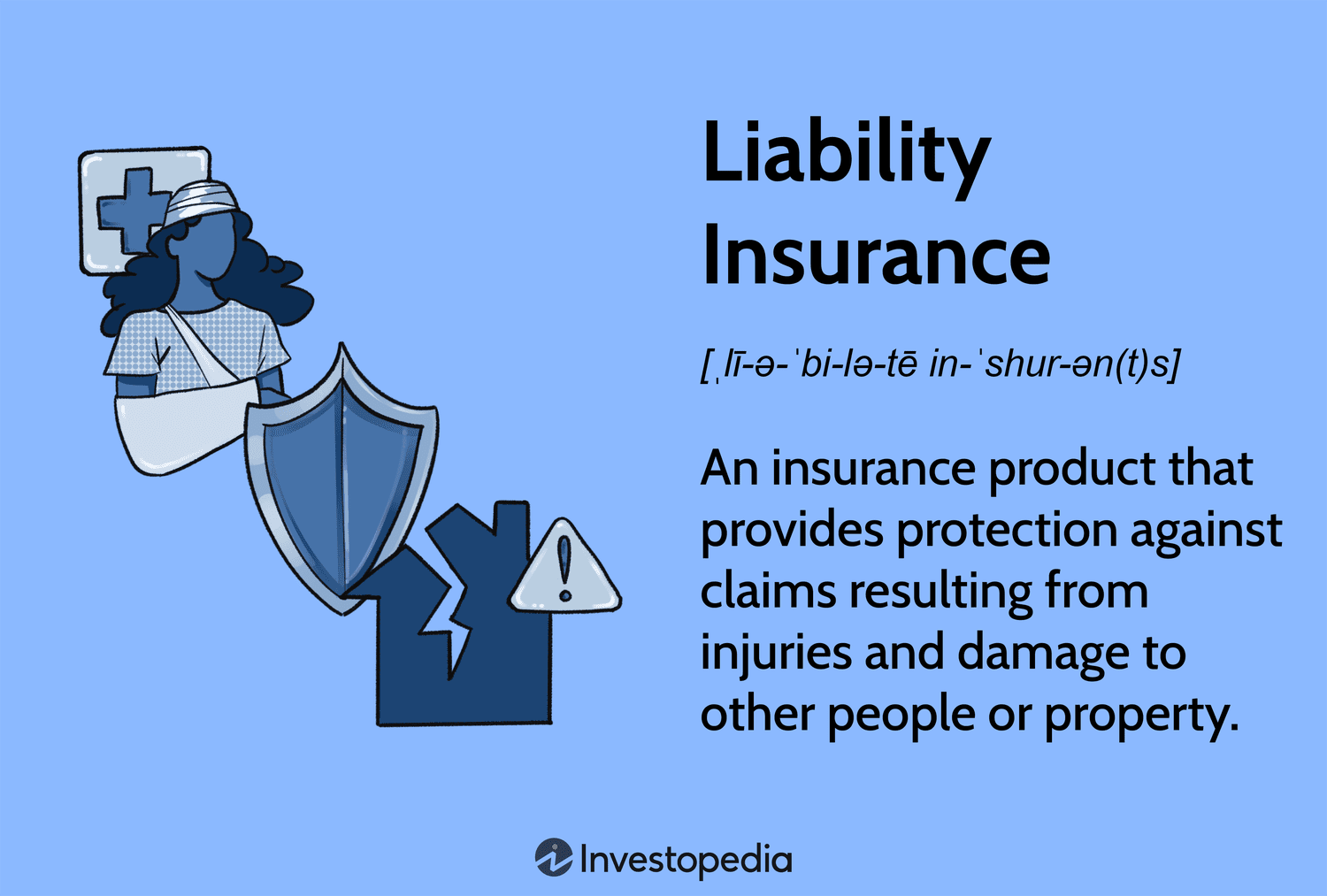

Liability Coverage

10 Million Dollar Business Insurance Policy

In the litigious society we live in, 10 Million Dollar Business Insurance Policy legal disputes can arise unexpectedly. Without adequate insurance, your business could face crippling legal costs. A Million Dollar Business Insurance Policy offers liability coverage, which can cover legal expenses, settlements, or judgments against your company, saving you from financial ruin.

Choosing the Right Policy

Tailoring to Your Needs

Not all businesses are the same, and neither are their insurance needs. When selecting a Million Dollar Business Insurance Policy, it’s essential to customize it to fit your specific industry and risks. Consult with insurance experts who can help you identify the coverage that best suits your business.

Evaluating Risk Factors

To determine the right coverage, you must assess the risk factors your business faces. Consider potential threats, such as the location of your business, industry-specific risks, and the size of your workforce. These factors will influence the level of coverage you require.

The Application Process

Working with Professionals

Applying for a Million Dollar Business Insurance Policy can be a complex process. It’s advisable to work closely with insurance professionals who can guide you through the application and underwriting process. Their expertise can ensure you receive the most comprehensive coverage possible.

Documentation and Disclosure

During the application process, be prepared to provide detailed information about your business, including financial records, safety protocols, and any previous insurance claims. Full disclosure is crucial to obtaining accurate coverage and preventing potential disputes in the future.

Benefits of a Million Dollar Business Insurance Policy

Financial Security

One of the most significant benefits of this policy is the peace of mind it provides. Knowing that your business is protected against substantial financial losses allows you to focus on growth and innovation without constantly worrying about potential risks.

Competitive Edge

Having robust insurance coverage can also enhance your business’s reputation. It demonstrates your commitment to responsible business practices and can make your company more attractive to partners, clients, and investors.

Tips for Managing Your Million Dollar Business Insurance Policy

Regular Reviews

Once you’ve secured a Million Dollar Business Insurance Policy, the work doesn’t end there. To ensure that your coverage remains relevant and effective, it’s essential to conduct regular policy reviews. As your business evolves, so do your risks. An annual review with your insurance professional can help identify any necessary adjustments in your coverage.

Risk Mitigation Strategies

While insurance provides a safety net, it’s also wise to implement risk mitigation strategies within your business. This proactive approach can help reduce the likelihood of claims and potentially lower your insurance premiums. It might include improving workplace safety, implementing robust cybersecurity measures, and adhering to industry-specific regulations.

Continuity Planning

In the unfortunate event of a disaster, having a business continuity plan in place is invaluable. This plan outlines how your company will continue its operations and recover after a significant disruption. Your Million Dollar Business Insurance Policy can play a crucial role in facilitating this recovery, but having a plan in advance can expedite the process.

Frequently Encountered Misconceptions

“I don’t need insurance; nothing will ever happen to my business.”

This common misconception can be financially devastating. Accidents and unforeseen events can affect any business, regardless of its size or industry. Insurance provides a safety net that no business should be without.

I can’t afford a Million Dollar Business Insurance Policy.

While insurance costs vary, it’s important to consider the potential financial impact of not having coverage. The cost of a policy is a fraction of what you might have to pay in the event of a significant loss or lawsuit.

Final Thoughts

Investing in a Million Dollar Business Insurance Policy is not just a prudent business decision; it’s a commitment to securing your company’s future. With the right coverage in place and a proactive risk management approach, you can confidently navigate the unpredictable landscape of the business world. Protecting your assets, reputation, and financial well-being should always be a top priority.

Exploring Additional Insurance Options

While the Million Dollar Business Insurance Policy offers comprehensive coverage, it’s essential to explore other insurance options that can complement and enhance your protection.

- Business Interruption Insurance

Business Interruption Insurance covers income losses that occur due to unexpected interruptions in your operations. Whether it’s a natural disaster, fire, or other unforeseen events that force your business to close temporarily, this coverage can help you recover lost income and operating expenses during downtime. - Cybersecurity Insurance

In today’s digital age, cybersecurity breaches are a real threat. Cybersecurity Insurance can protect your business from the financial consequences of data breaches, cyberattacks, and the associated legal liabilities. Given the increasing reliance on technology, this coverage is becoming more crucial than ever. - Key Person Insurance

If your business heavily relies on one or a few key individuals whose absence would severely impact operations, consider Key Person Insurance. This policy compensates your business for financial losses incurred if a vital team member becomes unable to work due to disability, illness, or death. - Commercial Auto Insurance

If your business uses vehicles for operations, Commercial Auto Insurance is a must. It covers accidents, injuries, and property damage related to your business vehicles. This insurance is essential, whether you have a single company car or an entire fleet.

The Evolving Landscape of Business Insurance

The world of insurance is continually evolving to adapt to new risks and challenges. It’s crucial to stay informed about emerging insurance trends and technologies that can further protect your business. Regularly consult with your insurance advisor to explore new options and ensure your coverage remains up-to-date.

Wrapping Up

In the complex and ever-changing landscape of business, safeguarding your financial investments and ensuring the continuity of your operations is paramount. A Million Dollar Business Insurance Policy serves as a solid foundation, but exploring complementary insurance options and staying proactive in risk management will provide comprehensive protection for your business.

Remember, insurance is not just a financial tool; it’s a strategic asset that can help your business thrive in the face of adversity.

Tips for Obtaining and Managing Your Million Dollar Business Insurance Policy

- Assess Your Needs Thoroughly

Before purchasing a Million Dollar Business Insurance Policy, conduct a comprehensive risk assessment. Identify potential threats to your business, whether they are natural disasters, legal liabilities, or other specific risks related to your industry. Understanding your needs is the first step in selecting the right coverage. - Work with an Experienced Broker

Choosing the right insurance broker or agent is crucial. Look for professionals experienced in commercial insurance and who understand your industry. They can help you navigate the complexities of insurance policies, find the best coverage, and negotiate competitive rates. - Review Policy Terms Carefully

When you receive your policy documents, don’t skim over them. Take the time to read and understand all the terms, conditions, and exclusions. If anything is unclear, ask your insurance provider for clarification. Knowing your policy inside and out will prevent surprises in the event of a claim. - Regularly Update Your Policy

As your business grows and evolves, so do your insurance needs. Regularly review your policy with your insurance advisor to ensure it still aligns with your business’s size and operations. Failing to update your coverage can leave you underinsured in critical areas. - Maintain Excellent Records

In case you need to file a claim, maintaining thorough and organized records is essential. Document all business transactions, safety protocols, and any incidents that could potentially lead to a claim. This documentation will be invaluable when processing a claim. - Implement Risk Management Practices

Insurance should not be your sole risk mitigation strategy. Implement robust risk management practices within your business. This can include safety training for employees, disaster preparedness plans, and cybersecurity measures. A proactive approach to risk can help reduce incidents and, in turn, insurance premiums. - Shop Around for Competitive Rates

Insurance rates can vary significantly between providers. Don’t hesitate to shop around and obtain quotes from multiple insurers. While cost is a factor, remember that the cheapest policy might not provide the coverage you need. Balance affordability with comprehensive protection. - Be Prepared for Claims

In the unfortunate event that you need to file a claim, know the claims process and have all the necessary documentation ready. Promptly report incidents to your insurer and follow their guidance closely. A well-handled claim can expedite the recovery process.

By following these tips, you can not only obtain the right Million Dollar Business Insurance Policy for your company but also manage it effectively to ensure that your business remains protected in all circumstances.

Remember, insurance is an investment in your business’s stability and longevity, and the effort you put into understanding and managing it can pay off significantly in times of need.

Handling Claims Effectively

- Prompt Reporting:

In the event of a covered incident, such as property damage or liability claim, notify your insurance provider promptly. Timely reporting is crucial as it initiates the claims process and allows the insurer to assess the situation promptly. - Provide Detailed Information:

When filing a claim, be thorough in providing all necessary information. Document the incident with photos, videos, or written descriptions. Include details of any injuries, damage, or losses. The more comprehensive your documentation, the smoother the claims process will be. - Cooperate Fully:

Work closely with your insurance adjuster and provide any requested documentation or information promptly. Cooperation is key to expediting the assessment and resolution of your claim. - Understand Your Responsibilities:

Familiarize yourself with your policy’s terms and conditions regarding claims. Be aware of any deductibles, coverage limits, or responsibilities you may have in the claims process.

Risk Mitigation and Prevention

- Safety Training:

Regularly conduct safety training for your employees. Educate them on best practices for accident prevention and emergency response. A safer workplace can lead to fewer claims. - Security Measures:

Invest in security measures like alarm systems, surveillance cameras, and cybersecurity solutions. These can deter potential incidents and reduce risks associated with theft, vandalism, or cyberattacks. - Disaster Preparedness:

Develop a comprehensive disaster preparedness plan that covers natural disasters, fires, and other emergencies. This plan should outline steps to protect your assets, ensure employee safety, and expedite recovery. - Legal Compliance:

Stay up-to-date with all relevant laws and regulations in your industry. Compliance can help prevent legal issues that may result in claims.

Policy Review and Adjustments

- Annual Policy Review:

Make it a habit to review your Million Dollar Business Insurance Policy annually. Changes in your business, such as growth or diversification, may require adjustments to your coverage. - Consult with Experts:

Consider seeking advice from insurance professionals who specialize in your industry. They can provide insights into emerging risks and recommend appropriate policy enhancements. - Evaluate Coverage Limits:

As your business assets and revenue grow, evaluate whether your policy’s coverage limits are still adequate. Adjustments may be necessary to ensure full protection.

Educating Your Team

- Employee Awareness:

Ensure your employees are aware of your insurance policies, especially those related to workplace safety and liability. Educated employees can play a role in preventing incidents. - Claims Reporting Process:

Train your staff on how to report incidents that could lead to claims. Establish clear protocols for reporting accidents, injuries, or property damage.

By diligently managing your Million Dollar Business Insurance Policy, practicing risk mitigation, and fostering a culture of safety within your company, you can maximize the benefits of your insurance coverage while minimizing potential risks.

Staying Informed

- Stay Current on Industry Trends:

Industries evolve, and new risks emerge over time. It’s vital to stay informed about developments in your industry that could affect your insurance needs. Attend industry conferences, join professional associations, and read industry publications to stay up-to-date. - Policy Renewal Alerts:

Set up reminders for policy renewal dates well in advance. This ensures that you have ample time to review your coverage and make any necessary adjustments. - Annual Premium Review:

Review your annual premiums to ensure they remain competitive. Don’t assume that your current insurer always offers the best rates. It’s worth shopping around periodically to see if you can get the same coverage for a lower premium.

Building a Strong Relationship with Your Insurer

- Open Communication:

Maintain open and transparent communication with your insurance provider. Share any changes in your business operations, locations, or assets promptly. This proactive approach can help prevent coverage gaps. - Claims History Review:

Regularly review your claims history with your insurer. Discuss ways to mitigate risks based on past incidents, and inquire about any potential premium reductions for maintaining a claims-free record. - Policy Updates:

Collaborate with your insurer to ensure your policy reflects your business’s current needs accurately. Regularly updating your policy can prevent overpayment for coverage you no longer require or underinsurance for new risks.

Employee Involvement

- Risk Awareness Training:

Educate your employees about the importance of risk management and safety practices. Encourage them to report potential risks or hazards they encounter in the workplace promptly. - Safety Committees:

Establish safety committees within your organization to identify and address potential risks proactively. Encourage employees to be active participants in maintaining a safe work environment.

Compliance and Regulation

- Compliance Checks:

Regularly audit your business operations to ensure compliance with local, state, and federal regulations. Non-compliance can lead to legal issues that may not be covered by your insurance. - Policy Adjustments for Regulatory Changes:

Be prepared to adjust your insurance policies if there are changes in regulations that affect your industry. Your insurer can help you navigate these changes.

Continual Learning

- Insurance Seminars and Workshops:

Consider attending insurance-related seminars and workshops to deepen your understanding of insurance principles, coverage options, and best practices in risk management.

Data Protection and Cybersecurity

- Data Backup and Recovery:

In today’s digital age, data is a critical asset. Implement robust data backup and recovery procedures to protect against data loss due to cyberattacks or technical failures. A cyber insurance policy can provide coverage for data breaches and related expenses. - Cybersecurity Training:

Train your employees to recognize and respond to potential cyber threats, such as phishing emails and malware. Educated employees can be your first line of defense against cyberattacks. - Regular Security Audits:

Conduct regular security audits and vulnerability assessments to identify and address weaknesses in your cybersecurity infrastructure. This proactive approach can help prevent costly data breaches.

Disaster Recovery Planning

- Business Continuity Planning:

Develop a comprehensive business continuity plan that outlines how your business will operate in the event of a disaster, whether it’s a natural disaster or a significant technical failure. Test this plan periodically to ensure it works effectively. - Insurance for Business Interruption:

Consider a Business Interruption Insurance policy, which can provide coverage for lost income and operating expenses during a period of business interruption. This coverage is crucial for maintaining financial stability during unforeseen disruptions.

Third-Party Liability

- Vendor and Contractor Liability:

Review the insurance coverage of vendors, suppliers, and contractors you work with. Ensure that they have adequate liability coverage, which can protect you in the event of any incidents involving their services or products. - Contractual Agreements:

When entering into contractual agreements with third parties, include clauses that require them to indemnify and hold your business harmless in case of any liabilities arising from their actions.

Environmental and Regulatory Compliance

- Environmental Liability:

If your business operations have the potential to impact the environment, consider Environmental Liability Insurance. This coverage can protect you from the costs associated with environmental cleanup and legal liabilities. - Regulatory Compliance:

Stay vigilant about compliance with environmental, safety, and industry-specific regulations. Non-compliance can lead to claims and penalties that may not be covered by your insurance.

Annual Risk Assessment

- Annual Risk Assessment:

Conduct an annual risk assessment to identify new risks, changes in business operations, or potential gaps in your insurance coverage. Address any emerging risks promptly.

Employee Benefits and Workers’ Compensation

- Employee Benefits Packages:

Consider offering competitive employee benefits packages. Adequate health, disability, and workers’ compensation coverage can enhance employee retention and satisfaction.

Legal Review

- Legal Counsel:

Consult with legal counsel to review your insurance policies and ensure they align with your business objectives and comply with current laws and regulations.

Ongoing Education

- Insurance Seminars and Workshops:

Continually educate yourself and key members of your team about insurance trends, coverage options, and best practices. This knowledge can help you make informed decisions about your policy.

Insurance Documentation and Records

- Document All Correspondence:

Maintain a well-organized file of all insurance-related correspondence, including policy documents, claims, and communications with your insurer. Having a clear record can be invaluable in case of disputes or when reviewing your coverage. - Policy Renewal Checklists:

Create a policy renewal checklist that includes key dates, required documents, and actions to take before renewing your policy. This checklist can help streamline the renewal process and ensure you don’t miss important details. - Digital Backup:

Consider digitizing your insurance documents and storing them securely in the cloud. This redundancy can protect against physical document loss due to fire, theft, or other disasters.

Professional Consultation

- Risk Management Experts:

Engage risk management experts or consultants who specialize in your industry. Their insights can help you identify and mitigate risks specific to your business, leading to more effective insurance coverage. - Legal Advisors:

Consult with legal advisors who can provide guidance on insurance-related legal matters, ensuring that your policies align with your business’s legal needs.

Compliance Audits

- Regular Compliance Audits:

Conduct regular compliance audits to ensure that your business adheres to all industry-specific regulations. Compliance can prevent unexpected claims and coverage issues.

Employee Wellness and Safety

- Employee Wellness Programs:

Implement employee wellness programs that promote a healthy workforce. Healthier employees are less likely to file health-related claims, which can positively impact your insurance premiums. - Safety Committees:

Empower safety committees within your organization to regularly assess workplace safety, identify hazards, and recommend improvements. Their proactive efforts can prevent accidents and claims.

Business Valuation

- Regular Business Valuations:

Consider periodic business valuations to ensure that your policy adequately covers your business’s current value. If your business has grown significantly, you may need to adjust your coverage limits.

Policy Benchmarking

- Benchmark Your Policy:

Periodically benchmark your insurance policy against industry standards and competitors. This can help you identify areas where you may need to enhance or adjust your coverage.

Claims Analysis

- Claims Analysis:

Analyze past insurance claims to identify trends and areas where you can proactively reduce risks. This data-driven approach can lead to better risk management strategies.

Employee Training

- Insurance Training for Employees:

Educate your employees about insurance and how it impacts the business. This awareness can encourage them to act responsibly and consider insurance implications in their roles.

Premium Payment Management

- Timely Premium Payments:

Ensure that you make premium payments on time. Late payments can lead to policy cancellations or lapses in coverage, leaving your business exposed to risks. - Payment Tracking:

Maintain a payment tracking system to monitor premium due dates. Set reminders to avoid missing payments, which can disrupt your coverage.

Insurance Policy Reviews

- Regular Policy Reviews:

Don’t wait for renewal to review your policy. Periodically assess your coverage to confirm that it aligns with your business’s current needs, assets, and operations. - Policy Endorsements:

Understand policy endorsements or add-ons that may enhance your coverage. These may include coverage for new assets, expanded operations, or emerging risks.

Alternative Risk Management Strategies

- Self-Insurance Consideration:

Depending on your business’s financial strength and risk tolerance, you might explore self-insurance options for certain risks. This involves setting aside funds to cover specific losses rather than relying solely on insurance. - Captive Insurance:

Evaluate whether establishing a captive insurance company (a subsidiary created to provide insurance to its parent company) is suitable for your business. Captive insurance can offer tailored coverage and potential cost savings.

Communication with Key Stakeholders

- Board and Shareholder Communication:

Keep your board of directors and shareholders informed about your insurance strategy, including any significant changes or new policies. Transparency can foster confidence and support in your risk management approach. - Employee Communication:

Continually communicate with your employees about safety measures, compliance, and their role in risk management. Engaged employees can contribute to a safer workplace and fewer claims.

Financial Planning

- Reserve Funds:

Set aside reserve funds for potential deductibles or unexpected costs associated with claims. Adequate financial planning can prevent financial strain when claims arise.

Industry-Specific Considerations

- Industry-Specific Risks:

Be mindful of industry-specific risks. Different sectors have unique challenges and liabilities, so tailor your insurance strategy to address these specific concerns.

Regulatory Compliance

- Regulatory Changes:

Stay vigilant about changes in local, state, and federal regulations that may impact your insurance requirements. Non-compliance can result in penalties and coverage gaps.

Disaster Response Planning

- Emergency Response Plan:

Regularly review and update your emergency response plan to ensure it aligns with your insurance coverage. Effective disaster response can mitigate losses and streamline the claims process.

Data Analytics and Predictive Modeling

- Data Analysis:

Embrace data analytics and predictive modeling tools to assess risk trends within your business. This data-driven approach can lead to proactive risk management and more accurate insurance coverage.

Continuing Education

- Insurance Education:

Invest in ongoing education for yourself and your team about insurance principles and best practices. This knowledge empowers you to make informed decisions about your policy.

Alternative Risk Transfer Strategies

- Risk Pools and Group Insurance:

Explore options for joining risk pools or group insurance programs relevant to your industry or business type. These arrangements can provide cost-effective coverage by spreading risks among multiple organizations. - Catastrophe Bonds:

In regions prone to natural disasters, consider catastrophe bonds as a way to transfer the risk of significant losses. These bonds provide funds in the event of specified catastrophic events, reducing your exposure.

Coverage Analysis

- Claims Scenario Testing:

Periodically conduct claims scenario testing with your insurer. This involves simulating potential claims to assess how your coverage would respond. Adjustments can be made based on these insights. - Sub-limits Evaluation:

Examine sub-limits within your insurance policy. Sub-limits may apply to specific risks, and you should ensure that they are adequate for your business’s needs.

Vendor and Supplier Risk Management

- Vendor Insurance Verification:

Verify that your vendors and suppliers have appropriate insurance coverage. Inadequate insurance on their part could potentially expose your business to liabilities. - Contractual Risk Mitigation:

Include contractual clauses that clearly define insurance requirements and indemnification terms in agreements with vendors and suppliers. These provisions can protect your interests in case of disputes.

Coverage for Emerging Risks

- Emerging Risk Assessment:

Stay vigilant about emerging risks in your industry, such as cybersecurity threats, environmental concerns, or new regulations. Evaluate your insurance policy to ensure it addresses these evolving risks adequately.

Employee Engagement

- Employee Training and Reporting:

Encourage employees to actively participate in risk management. Provide training on identifying and reporting potential hazards, creating a safer work environment. - Whistleblower Programs:

Establish confidential whistleblower programs that allow employees to report concerns without fear of retaliation. Early reporting can prevent claims and legal issues.

Insurance Technology

- Insurtech Integration:

Explore the integration of insurtech solutions into your insurance management process. These technologies can streamline policy administration, claims processing, and risk assessment.

Environmental and Sustainability Focus

- Sustainable Practices:

Incorporate sustainable practices into your business operations. Demonstrating a commitment to environmental responsibility can positively impact your insurance risk profile.

Resilience Testing

- Scenario Planning:

Conduct scenario planning exercises to test your business’s resilience to various risks, including natural disasters, economic downturns, and market fluctuations.

Benchmarking and Peer Comparison

- Peer Benchmarking:

Compare your insurance coverage and risk management strategies with industry peers. Benchmarking can reveal best practices and areas where improvements may be needed.

Legal Risk Assessments

- Regular Legal Audits:

Conduct regular legal audits to identify potential legal liabilities that might not be covered by insurance. Address these issues proactively.

International Considerations

- Global Operations:

If your business operates internationally, be aware of the unique insurance requirements and regulations in each country. Ensure that your insurance policies cover global operations adequately.

Continuous Improvement

- Continuous Feedback:

Encourage feedback from employees, customers, and other stakeholders regarding safety and risk management. Use this feedback to make continuous improvements in your risk mitigation strategies.

Loss Control Programs

- Specialized Loss Control Measures:

Collaborate with loss control specialists to implement specialized safety and risk reduction programs tailored to your industry. These experts can provide insights into industry-specific risks and mitigation strategies. - Predictive Analytics for Loss Control:

Utilize predictive analytics to identify potential areas of loss and proactively implement measures to mitigate them. Data-driven insights can help you target risk reduction efforts effectively.

Enterprise Risk Management (ERM)

- ERM Framework:

Develop an Enterprise Risk Management framework that integrates risk assessment, risk monitoring, and mitigation strategies across all aspects of your business. ERM provides a comprehensive view of your risk landscape. - ERM Software Tools:

Consider implementing ERM software tools that streamline risk assessment and management processes, allowing for real-time monitoring and reporting.

Business Continuity Testing

- Stress Testing:

Conduct stress tests and scenario-based simulations to evaluate the resilience of your business continuity plans. Identify weaknesses and make improvements to ensure rapid recovery in the face of significant disruptions. - Supplier and Vendor Continuity:

Assess the continuity plans of your critical suppliers and vendors. A disruption in their operations can impact your business, so ensure they have robust continuity measures in place.

Strategic Insurance Review

- Strategic Policy Analysis:

Engage with insurance experts to conduct a strategic analysis of your insurance policies. Assess how well they align with your business’s long-term goals and potential growth strategies. - Policy Layering:

Explore the concept of policy layering, which involves combining multiple insurance policies to create a comprehensive risk management strategy. This approach can optimize coverage while managing costs.

Alternative Risk Financing

- Risk Retention and Self-Insurance:

Develop a risk retention strategy, including self-insurance options, where you set aside funds to cover expected losses. This approach can provide more control over your insurance costs. - Risk Pools and Risk Captives:

Investigate the possibility of joining industry-specific risk pools or establishing a risk captive to share and manage risks collectively with other organizations in your sector.

Advanced Technology Integration

- Blockchain for Insurance:

Explore blockchain technology for insurance management, which can enhance transparency, reduce fraud, and streamline claims processing. - IoT and Telematics:

Leverage the Internet of Things (IoT) and telematics for risk monitoring. These technologies can provide real-time data on equipment health, vehicle safety, and more.

International Risk Management

- Global Risk Assessment:

If your business operates internationally, conduct comprehensive global risk assessments. Understand the unique risks and insurance requirements in each country of operation. - Global Policy Coordination:

Coordinate your insurance policies across borders to ensure seamless coverage and compliance with international regulations.

Ethical Risk Management

- Ethical Business Practices:

Emphasize ethical business practices and corporate responsibility as part of your risk management strategy. Unethical behavior can lead to legal issues and reputational damage.

Sustainability and ESG Integration

- ESG (Environmental, Social, and Governance) Considerations:

Integrate ESG principles into your risk management strategy. This involves assessing how environmental, social, and governance factors can impact your business and insurance needs. Insurers increasingly consider ESG practices when underwriting policies, so demonstrating a commitment to sustainability can lead to better terms and rates.

Risk Modeling and Analytics

- Advanced Risk Modeling:

Invest in advanced risk modeling and analytics tools. These tools can provide more accurate assessments of your business’s unique risks and help you make data-driven decisions regarding coverage and risk mitigation.

Parametric Insurance

- Parametric Insurance Solutions:

Explore parametric insurance options, which pay out based on predefined triggers such as weather events, seismic activity, or economic indicators. These policies offer rapid and transparent claims processing, minimizing downtime and financial losses.

Cybersecurity Resilience

- Cybersecurity Resilience Assessments:

Conduct regular cybersecurity resilience assessments to identify vulnerabilities and areas for improvement. Cyber insurance is essential in today’s digital landscape, but a proactive approach to cybersecurity can reduce the likelihood of cyber incidents.

Captive Insurance

- Captives for Specific Risks:

Consider setting up a captive insurance company to cover specific risks that are unique to your business. Captives provide more control over risk management and can offer cost savings over time.

Contingency Planning

- Contingency Plans for Supply Chain Disruptions:

Develop comprehensive contingency plans to address supply chain disruptions, which can have cascading effects on your business. Insurance coverage and risk mitigation strategies should be aligned with these plans.

Crisis Management

- Crisis Management Teams:

Establish crisis management teams within your organization, with clearly defined roles and responsibilities. These teams should be prepared to respond swiftly to major incidents, working in coordination with insurers and other stakeholders.

Reputation Risk Management

- Reputation Risk Assessments:

Implement reputation risk assessments to evaluate how potential events and crises could impact your brand and public perception. Mitigation strategies, including crisis communication plans, should be in place to safeguard your reputation.

Customized Coverage

- Tailored Coverage Options:

Work closely with insurers to create customized coverage options that align precisely with your business’s unique risks. Don’t settle for one-size-fits-all policies when your risks are specific.

Employee Training and Engagement

- Advanced Employee Training:

Provide advanced training to employees on risk awareness, ethical conduct, and compliance. Engaged and educated employees can play a significant role in risk mitigation.

Continuous Evaluation

- Continuous Improvement Framework:

Implement a continuous improvement framework for your risk management and insurance strategies. Regularly evaluate the effectiveness of your measures and adjust them as needed.

Strategic Risk Financing

- Risk Financing Optimization:

Collaborate with risk management experts to optimize your risk financing strategy. This involves finding the right balance between risk retention, risk transfer, and risk mitigation to minimize overall costs while maintaining comprehensive coverage.

Insurance Technology (Insurtech) Advancements

- Blockchain for Claims Processing:

Explore blockchain applications for streamlining claims processing. Blockchain can enhance transparency, reduce fraud, and accelerate claims settlements, ensuring quicker recovery from covered incidents. - AI and Predictive Analytics:

Leverage artificial intelligence (AI) and predictive analytics to assess risks and identify trends. Advanced algorithms can help you proactively manage risks and adjust your insurance strategy accordingly.

Multinational Insurance Strategies

- Global Insurance Programs:

If your business operates internationally, consider implementing a global insurance program. This centralizes your insurance coverage, streamlines administration, and ensures consistency in coverage across different regions. - Local Compliance Expertise:

Partner with local experts or brokers in each country of operation who possess in-depth knowledge of local insurance regulations. Compliance with these regulations is crucial to avoid fines and coverage gaps.

Reputation and Brand Protection

- Brand Resilience Plans:

Develop brand resilience plans that outline strategies for maintaining a positive brand image during crises. These plans should align with your insurance coverage to ensure comprehensive protection.

Data Privacy and Cybersecurity

- Advanced Cybersecurity Measures:

Continuously update and enhance your cybersecurity measures to protect sensitive data. Cyber insurance policies should be reviewed and adjusted to address evolving cyber threats.

ERM Integration

- ERM Integration with Strategic Planning:

Integrate Enterprise Risk Management (ERM) into your strategic planning process. ERM should inform decision-making at all levels, ensuring that your insurance strategy aligns with your business goals.

Advanced Legal Risk Management

- Legal Risk Mitigation:

Collaborate closely with legal advisors to identify and mitigate legal risks. This includes assessing contracts, intellectual property protection, and compliance with industry-specific regulations.

Scenario-Based Testing

- Advanced Scenario Testing:

Expand your scenario-based testing to encompass a wider range of potential disruptions, including global events, economic crises, and geopolitical risks. These tests help you refine your risk management and insurance strategies.

Comprehensive Supply Chain Resilience

- End-to-End Supply Chain Resilience:

Develop end-to-end supply chain resilience strategies that address every link in your supply chain. Insurance should cover potential disruptions at each stage.

Collaborative Risk Management

- Stakeholder Collaboration:

Collaborate with all stakeholders, including suppliers, customers, and insurers, in a proactive approach to risk management. Transparent communication and shared risk assessment can lead to mutually beneficial solutions.

Continuous Learning and Adaptation

- Continuous Learning Culture:

Foster a culture of continuous learning within your organization. Stay informed about emerging risks, insurance trends, and industry-specific challenges to adapt your strategy accordingly.

Strategic Vendor Partnerships

- Strategic Vendor Relationships:

Establish long-term partnerships with insurers, brokers, and risk management firms. These relationships can provide you with access to the latest industry insights, customized solutions, and preferential terms. - Risk Pooling with Vendors:

Consider risk-sharing arrangements with key vendors and suppliers. Collaborative risk pooling can help distribute the financial burden of insurance premiums and claims.

Advanced Claims Management

- Advanced Claims Analytics:

Implement advanced claims analytics to gain deeper insights into your claims history. This data can uncover patterns, helping you refine your risk management and insurance strategies. - Claims Benchmarking:

Benchmark your claims experience against industry peers. This can highlight areas where you might be able to improve safety and reduce claims, ultimately leading to lower premiums.

Climate Risk Assessment

- Climate Risk Modeling:

In the face of increasing climate-related risks, invest in climate risk modeling to assess how climate change might impact your business. This can inform your insurance decisions and adaptation strategies.

Regulatory Risk Management

- Regulatory Compliance Assessments:

Regularly assess your compliance with industry-specific regulations. Any non-compliance could result in claims that your insurance policy might not cover. - Regulatory Change Monitoring:

Stay vigilant about changes in regulations that affect your industry. A proactive approach to adapting your insurance coverage can prevent gaps in protection.

Emerging Risk Identification

- Risk Forecasting:

Leverage advanced risk forecasting tools and methodologies. These can help identify emerging risks, such as geopolitical instability, technological disruption, or global health crises.

Third-Party Risk Management

- Comprehensive Due Diligence:

Conduct comprehensive due diligence when entering into partnerships or collaborations with third parties. This includes assessing their insurance coverage and risk management practices.

Employee Empowerment

- Empowering Risk Champions:

Empower employees at all levels to become risk champions within your organization. Encourage them to actively identify and report risks, fostering a culture of shared responsibility.

Data Privacy Compliance

- GDPR and Data Privacy Compliance:

If your business deals with personal data, ensure compliance with data privacy regulations like GDPR. Violations can lead to costly legal actions that insurance might not fully cover.

Environmental Stewardship

- Environmental Impact Reduction:

Pursue initiatives to reduce your environmental footprint. Insurers may offer incentives or discounts for environmentally responsible practices.

Resilience Certification

- Business Resilience Certification:

Pursue business resilience certifications such as ISO 22301. These certifications demonstrate your commitment to resilience and may positively influence insurance terms.

Continuous Board Involvement

- Board Risk Oversight:

Ensure that your board of directors is actively involved in risk oversight. Their guidance and expertise can contribute significantly to the effectiveness of your insurance strategy.

Continuous Review and Adaptation

- Regular Risk Assessments:

Conduct regular, comprehensive risk assessments that encompass both internal and external factors. Continuously adapt your insurance strategy to align with evolving risks and business objectives.

Strategic Risk Transfer

- Structured Risk Transfer:

Work with insurers to develop structured risk transfer solutions. This may involve creating bespoke policies or alternative risk transfer mechanisms tailored to your business’s unique risk profile.

Business Interruption Coverage

- Extended Business Interruption Coverage:

Assess the need for extended business interruption coverage. This can help mitigate the financial impact of prolonged disruptions, such as those caused by global events or supply chain interruptions.

Artificial Intelligence (AI) Integration

- AI for Risk Assessment:

Integrate AI and machine learning into your risk assessment processes. AI can analyze vast amounts of data to identify emerging risks and trends that human analysis may overlook.

Parametric Insurance Expansion

- Parametric Insurance for Non-Physical Losses:

Explore the use of parametric insurance for non-physical losses, such as revenue fluctuations due to adverse weather conditions or other predefined triggers.

Advanced Cybersecurity

- Advanced Threat Detection:

Implement advanced threat detection technologies to identify and respond to cyber threats in real-time. This can reduce the likelihood and severity of cyber-related claims.

Strategic Captive Management

- Captive Insurance Optimization:

If you have a captive insurance company, regularly review its performance and assess its alignment with your business’s evolving needs. Adjust the captive’s strategy and structure as necessary.

Vendor Risk Management

- Vendor Risk Mitigation:

Strengthen your vendor risk management program by conducting regular assessments, monitoring vendor compliance, and requiring higher insurance coverage from critical vendors.

Stakeholder Engagement

- Stakeholder Risk Collaboration:

Engage with stakeholders—including customers, investors, and regulatory bodies—on risk management. Transparency and collaboration can enhance your risk mitigation efforts.

Regulatory Advocacy

- Industry Regulatory Advocacy:

Participate in industry associations and advocate for regulatory changes that can benefit your business. Align your insurance strategies with anticipated regulatory shifts.

Geopolitical Risk Assessment

- Geopolitical Risk Analysis:

Stay informed about geopolitical developments that could affect your business, especially if you operate internationally. Adjust your insurance strategy to address geopolitical risks.

Sustainability Reporting

- Enhanced Sustainability Reporting:

Enhance your sustainability reporting practices, showcasing your commitment to environmental and social responsibility. This can positively influence insurers and stakeholders.

Pandemic Preparedness

- Advanced Pandemic Planning:

Develop advanced pandemic preparedness plans that incorporate lessons learned from global events. Ensure your insurance policies provide adequate coverage for pandemic-related disruptions.

Reinsurance Optimization

- Reinsurance Strategy Enhancement:

Collaborate with reinsurers to optimize your reinsurance strategy. Adjust the layers and terms to align with your risk appetite and financial goals.

Ethical Risk Audits

- Ethical Risk Audits:

Conduct ethical risk audits to identify potential ethical and compliance risks within your business. Address these risks proactively to avoid legal and reputational issues.

Continuous Learning Culture

- Risk Management Education:

Foster a continuous learning culture related to risk management within your organization. Regular training and awareness programs can empower employees to contribute to risk mitigation.

Regulatory Advocacy

- Active Engagement with Regulators:

Go beyond compliance by actively engaging with regulators in your industry. Advocate for policies that create a favorable insurance landscape for your business while aligning with broader industry goals.

Emerging Risk Assessment

- Scenario-Based Risk Assessments:

Conduct scenario-based risk assessments that simulate complex and multifaceted risks. This approach can reveal vulnerabilities that may not be apparent in standard risk assessments.

Business Continuity Testing

- Advanced Business Continuity Testing:

Elevate your business continuity testing by including more realistic and complex scenarios. Simulate disruptions that challenge your organization’s resilience to the fullest extent.

Diversified Insurance Portfolio

- Diversified Insurance Providers:

Diversify your insurance portfolio by working with multiple insurers, both large and niche players. This strategy can enhance your negotiating power and spread risk effectively.

Alternative Risk Financing

- Risk-Linked Securities:

Explore risk-linked securities such as catastrophe bonds and insurance-linked securities (ILS). These instruments allow you to transfer specific risks to capital markets.

Predictive Supply Chain Management

- Predictive Supply Chain Analytics:

Leverage predictive analytics to manage supply chain risks proactively. Identify potential disruptions and optimize your supply chain to minimize exposure.

Cross-Functional Risk Teams

- Integrated Risk Teams:

Form cross-functional risk teams that include experts from various departments within your organization. Collaborative risk assessment can yield more holistic insights.

ESG Integration in Insurance

- ESG Metrics in Insurance:

Integrate Environmental, Social, and Governance (ESG) metrics into your insurance strategies. Align your coverage with sustainable practices to mitigate reputational and environmental risks.

Crisis Simulation Exercises

- Advanced Crisis Simulations:

Conduct advanced crisis simulation exercises that involve real-time decision-making and coordination across all levels of your organization.

Strategic Reevaluation

- Periodic Strategic Reevaluation:

Regularly reevaluate your long-term strategic goals and how they align with your insurance coverage. Adjust your policies and strategies accordingly.

Cybersecurity Maturity

- Cybersecurity Maturity Framework:

Implement a cybersecurity maturity framework that goes beyond compliance to assess and enhance your organization’s cybersecurity resilience.

Talent Development

- In-House Expertise:

Invest in developing in-house insurance and risk management expertise. This can lead to more effective risk management and better negotiation with insurers.

International Risk Coordination

- Global Risk Coordination:

If your business operates internationally, establish a global risk coordination team to ensure consistency in risk management practices across borders.

Disruptive Technology Adoption

- Adoption of Emerging Technologies:

Stay at the forefront of disruptive technologies such as blockchain, artificial intelligence, and quantum computing. These technologies can impact insurance and risk management.

Continuous Improvement Culture

- Kaizen Approach:

Foster a culture of continuous improvement within your organization. Encourage employees to identify areas for enhancement in risk management and insurance practices.

Advanced Risk Communication

- Advanced Risk Communication:

Enhance your risk communication strategies to engage stakeholders effectively during times of crisis. Transparency and clear messaging are essential.

Sustainable Partnerships

- Sustainable Vendor Relationships:

Collaborate with vendors and partners who share your commitment to sustainability and ethical practices. Ethical supply chains can reduce reputational and legal risks.

Risk Culture Development

- Risk Culture Enhancement:

Foster a risk-aware culture throughout your organization. Encourage all employees to actively participate in risk management, from frontline staff to top executives.

Resilience Enhancement

- Resilience Training:

Invest in resilience training for employees at all levels. Equip them with the skills to adapt and respond effectively to unforeseen challenges.

Predictive Analytics in Claims

- Predictive Analytics for Claims Processing:

Implement predictive analytics in claims processing to identify potential fraudulent claims early and streamline legitimate claims efficiently.

Advanced Risk Metrics

- Advanced Risk Metrics:

Develop and track advanced risk metrics that go beyond traditional key performance indicators (KPIs). These metrics can provide more nuanced insights into your risk landscape.

ERM Software Integration

- ERM Software Integration:

Integrate Enterprise Risk Management (ERM) software that offers real-time risk monitoring and reporting capabilities. This allows for proactive risk mitigation.

Regulatory Sandbox Participation

- Regulatory Sandbox Participation:

Explore opportunities to participate in regulatory sandboxes, where you can test innovative risk management and insurance solutions within a controlled environment.

AI for Claims Assessment

- AI-Powered Claims Assessment:

Utilize artificial intelligence to assess claims. AI can analyze large datasets and patterns, helping to validate claims more efficiently.

Advanced Contingency Planning

- Complex Contingency Planning:

Develop contingency plans for complex scenarios, such as global supply chain disruptions or large-scale cyberattacks. These plans should be tested rigorously.

Insurtech Partnerships

- Strategic Insurtech Collaborations:

Collaborate with insurtech startups to leverage their innovative technologies for risk assessment, policy administration, and claims management.

Scenario Modeling

- Advanced Scenario Modeling:

Enhance your scenario modeling capabilities to consider a wider range of risk factors, including geopolitical events, technological advancements, and social trends.

M&A Risk Assessment

- M&A Risk Assessment:

If your business is involved in mergers and acquisitions, conduct comprehensive risk assessments of target companies to identify potential liabilities and insurance needs.

Climate Risk Disclosure

- Advanced Climate Risk Disclosure:

Go beyond basic climate risk reporting by providing detailed information on how your organization plans to address climate-related challenges.

Global Legal Compliance

- Global Legal Compliance:

Ensure that your insurance policies comply with a wide range of international legal requirements, especially if your business operates in multiple countries.

Strategic Risk Sourcing

- Strategic Risk Sourcing:

Evaluate the most cost-effective methods for sourcing insurance coverage, which could include captives, consortiums, or self-insurance options.

Environmental Certification

- Environmental Certification:

Pursue environmental certifications such as ISO 14001 to demonstrate your commitment to sustainable practices and reduce environmental risks.

Continuous Stakeholder Engagement

- Stakeholder Risk Dialogues:

Maintain ongoing dialogues with stakeholders, including customers, investors, and regulators, to address their risk-related concerns and expectations.

Conclusion

In the world of business, securing your success is as important as achieving it. A Million Dollar Business Insurance Policy acts as a sturdy safety net, protecting your assets, reputation, and financial well-being. By customizing your coverage, understanding your risk factors, and working with experts, you can ensure that your business continues to thrive, even in the face of adversity.

Remember, your insurance policy is an investment in the future of your business, offering peace of mind and financial security in times of adversity. Properly managed, it can be a valuable asset that supports your long-term success.

FAQ

- What does a Million Dollar Business Insurance Policy typically cover?

A Million Dollar Business Insurance Policy usually covers a wide range of risks, including property damage, liability claims, legal expenses, and more. The specific coverage can be tailored to your business’s needs. - Is this insurance policy suitable for startups and small businesses?

Yes, startups and small businesses can benefit from this policy, especially as they grow. It provides financial security and protection against unexpected events that could otherwise cripple a young business. - How much does a Million Dollar Business Insurance Policy cost?

The cost varies depending on factors like your industry, location, and the coverage you need. It’s essential to work with an insurance professional to get an accurate quote. - Can I change my coverage as my business grows?

Yes, you can adjust your coverage to accommodate your business’s growth and changing needs. Regularly reviewing your policy with an insurance expert is a good practice. - Where can I get more information about obtaining a Million Dollar Business Insurance Policy?

For more information and assistance in obtaining this insurance policy, please visit